Energy Balance Off Gas Utilization and Heat Recovery in Hydrogen DRI

AUG 25, 20259 MIN READ

Generate Your Research Report Instantly with AI Agent

Patsnap Eureka helps you evaluate technical feasibility & market potential.

Hydrogen DRI Technology Background and Objectives

Direct Reduced Iron (DRI) production using hydrogen as a reducing agent represents a transformative approach in the steel industry's decarbonization journey. This technology has evolved significantly over the past decades, transitioning from experimental concepts to commercially viable solutions. The fundamental principle involves using hydrogen to remove oxygen from iron ore, producing metallic iron without the carbon emissions associated with traditional blast furnace processes.

The historical development of hydrogen-based DRI began in the 1970s with initial research efforts, gaining momentum in the 1990s as environmental concerns grew. However, it wasn't until the 2010s that significant commercial interest emerged, driven by increasingly stringent carbon emission regulations and the global push toward sustainable industrial practices.

Current hydrogen DRI technology faces critical challenges in energy efficiency, particularly regarding off-gas utilization and heat recovery. Traditional DRI processes generate substantial waste heat and process gases that, if properly captured and reused, could significantly improve overall energy balance and economic viability. The technology aims to achieve near-zero carbon emissions while maintaining or improving production efficiency compared to conventional methods.

The primary technical objective in hydrogen DRI development is optimizing the energy balance through innovative off-gas utilization strategies and advanced heat recovery systems. This involves capturing thermal energy from various process stages and recycling hydrogen-rich off-gases back into the reduction process, thereby creating a more closed-loop system with minimal energy wastage.

Market drivers for this technology include increasingly stringent carbon pricing mechanisms, growing consumer demand for green steel products, and corporate sustainability commitments across the value chain. The European Union's carbon border adjustment mechanism and similar policies worldwide are accelerating investment in low-carbon steelmaking technologies.

The technology roadmap envisions progressive improvements in energy efficiency, with near-term goals focusing on hybrid systems that combine natural gas and hydrogen, while mid-term objectives target complete hydrogen-based reduction with advanced energy recovery. Long-term aspirations include fully integrated systems with renewable hydrogen production and near-perfect energy circularity.

Success in this field requires interdisciplinary collaboration between metallurgical engineering, thermal management systems, process control technologies, and renewable energy integration. The ultimate goal is developing economically viable hydrogen DRI systems that can operate at industrial scale with minimal carbon footprint, positioning steel production for sustainability in a carbon-constrained future.

The historical development of hydrogen-based DRI began in the 1970s with initial research efforts, gaining momentum in the 1990s as environmental concerns grew. However, it wasn't until the 2010s that significant commercial interest emerged, driven by increasingly stringent carbon emission regulations and the global push toward sustainable industrial practices.

Current hydrogen DRI technology faces critical challenges in energy efficiency, particularly regarding off-gas utilization and heat recovery. Traditional DRI processes generate substantial waste heat and process gases that, if properly captured and reused, could significantly improve overall energy balance and economic viability. The technology aims to achieve near-zero carbon emissions while maintaining or improving production efficiency compared to conventional methods.

The primary technical objective in hydrogen DRI development is optimizing the energy balance through innovative off-gas utilization strategies and advanced heat recovery systems. This involves capturing thermal energy from various process stages and recycling hydrogen-rich off-gases back into the reduction process, thereby creating a more closed-loop system with minimal energy wastage.

Market drivers for this technology include increasingly stringent carbon pricing mechanisms, growing consumer demand for green steel products, and corporate sustainability commitments across the value chain. The European Union's carbon border adjustment mechanism and similar policies worldwide are accelerating investment in low-carbon steelmaking technologies.

The technology roadmap envisions progressive improvements in energy efficiency, with near-term goals focusing on hybrid systems that combine natural gas and hydrogen, while mid-term objectives target complete hydrogen-based reduction with advanced energy recovery. Long-term aspirations include fully integrated systems with renewable hydrogen production and near-perfect energy circularity.

Success in this field requires interdisciplinary collaboration between metallurgical engineering, thermal management systems, process control technologies, and renewable energy integration. The ultimate goal is developing economically viable hydrogen DRI systems that can operate at industrial scale with minimal carbon footprint, positioning steel production for sustainability in a carbon-constrained future.

Market Analysis for Green Steel Production

The global steel industry is experiencing a significant shift towards greener production methods, driven by increasing environmental regulations and corporate sustainability commitments. The market for green steel production, particularly using hydrogen-based direct reduced iron (H-DRI) technology, is projected to grow substantially over the next decade. Current estimates value the green steel market at approximately $2.2 billion in 2023, with expectations to reach $27 billion by 2032, representing a compound annual growth rate of 28.5%.

European markets are leading this transition, with countries like Sweden, Germany, and Austria at the forefront of implementing hydrogen-based steelmaking technologies. The EU's carbon border adjustment mechanism and stringent emission reduction targets have created strong market incentives for steel producers to adopt cleaner technologies. Asian markets, particularly China and Japan, are also making significant investments in green steel research and development, though implementation remains at earlier stages compared to Europe.

Consumer demand for green steel is primarily driven by automotive, construction, and renewable energy sectors. Premium pricing for green steel products currently ranges between 10-30% above conventional steel, though this premium is expected to decrease as technologies mature and economies of scale are achieved. Major automotive manufacturers have already committed to incorporating green steel into their supply chains, with some pledging to use only carbon-neutral steel by 2040.

Energy balance optimization in hydrogen DRI processes represents a critical factor in market adoption. The ability to effectively utilize off-gases and recover heat directly impacts production costs, which remain the primary barrier to widespread market penetration. Steel producers that can demonstrate superior energy efficiency in their H-DRI processes gain significant competitive advantage in this emerging market.

Investment trends show increasing capital allocation toward green steel technologies, with venture capital and corporate investment in the sector exceeding $5 billion in 2022 alone. Government subsidies and green financing initiatives are further accelerating market growth, particularly in regions with ambitious decarbonization targets.

Market forecasts indicate that by 2030, hydrogen-based steel production could account for approximately 12% of global steel output, with this percentage rising significantly by 2050 as technology costs decrease and carbon pricing mechanisms become more widespread. The market for technologies specifically focused on energy recovery and off-gas utilization within hydrogen DRI systems is expected to develop into a specialized sub-sector worth an estimated $3.5 billion by 2028.

European markets are leading this transition, with countries like Sweden, Germany, and Austria at the forefront of implementing hydrogen-based steelmaking technologies. The EU's carbon border adjustment mechanism and stringent emission reduction targets have created strong market incentives for steel producers to adopt cleaner technologies. Asian markets, particularly China and Japan, are also making significant investments in green steel research and development, though implementation remains at earlier stages compared to Europe.

Consumer demand for green steel is primarily driven by automotive, construction, and renewable energy sectors. Premium pricing for green steel products currently ranges between 10-30% above conventional steel, though this premium is expected to decrease as technologies mature and economies of scale are achieved. Major automotive manufacturers have already committed to incorporating green steel into their supply chains, with some pledging to use only carbon-neutral steel by 2040.

Energy balance optimization in hydrogen DRI processes represents a critical factor in market adoption. The ability to effectively utilize off-gases and recover heat directly impacts production costs, which remain the primary barrier to widespread market penetration. Steel producers that can demonstrate superior energy efficiency in their H-DRI processes gain significant competitive advantage in this emerging market.

Investment trends show increasing capital allocation toward green steel technologies, with venture capital and corporate investment in the sector exceeding $5 billion in 2022 alone. Government subsidies and green financing initiatives are further accelerating market growth, particularly in regions with ambitious decarbonization targets.

Market forecasts indicate that by 2030, hydrogen-based steel production could account for approximately 12% of global steel output, with this percentage rising significantly by 2050 as technology costs decrease and carbon pricing mechanisms become more widespread. The market for technologies specifically focused on energy recovery and off-gas utilization within hydrogen DRI systems is expected to develop into a specialized sub-sector worth an estimated $3.5 billion by 2028.

Off-Gas Recovery Challenges in H2-DRI Processes

The recovery and utilization of off-gases in Hydrogen-based Direct Reduced Iron (H2-DRI) processes present significant technical challenges that must be addressed to optimize energy efficiency and reduce environmental impact. The primary off-gases in these processes include unreacted hydrogen, carbon monoxide, carbon dioxide, water vapor, and trace contaminants, each requiring specific handling approaches.

Temperature management represents one of the most critical challenges in off-gas recovery. The gases exit the reduction furnace at temperatures ranging from 800°C to 950°C, necessitating sophisticated heat exchange systems that can withstand these extreme conditions while efficiently transferring thermal energy. Material selection for these systems must account for potential hydrogen embrittlement, high-temperature corrosion, and thermal cycling stresses.

Contamination issues further complicate recovery efforts. Off-gases typically contain particulate matter, including iron dust and other mineral contaminants that can foul heat exchangers, catalysts, and gas separation membranes. These contaminants reduce system efficiency and increase maintenance requirements, necessitating robust filtration systems that themselves must operate at elevated temperatures.

Pressure management presents another significant challenge. The pressure differentials throughout the DRI process must be carefully controlled to maintain process stability while enabling efficient gas recovery. Pressure drops across filtration and heat recovery systems must be minimized to reduce the energy required for gas recirculation, which directly impacts the overall energy balance of the process.

Hydrogen separation and purification represent perhaps the most technically demanding aspect of off-gas recovery. Current technologies, including Pressure Swing Adsorption (PSA), membrane separation, and cryogenic distillation, each have limitations when applied to the specific conditions of DRI off-gases. PSA systems struggle with the temperature and contaminant profiles, membrane systems face durability challenges in these harsh environments, and cryogenic approaches require significant energy inputs that may offset recovery benefits.

System integration challenges arise when attempting to incorporate off-gas recovery into existing DRI plant designs. The intermittent nature of some DRI operations creates fluctuating off-gas volumes and compositions, requiring recovery systems with sufficient flexibility to handle these variations while maintaining efficiency. Additionally, the physical space constraints in existing facilities often limit retrofit options for comprehensive recovery systems.

Economic barriers further complicate implementation, as the capital expenditure for advanced recovery systems must be justified through operational savings or regulatory compliance. The return on investment calculations must account for maintenance costs, system reliability, and the market value of recovered energy and gases.

Temperature management represents one of the most critical challenges in off-gas recovery. The gases exit the reduction furnace at temperatures ranging from 800°C to 950°C, necessitating sophisticated heat exchange systems that can withstand these extreme conditions while efficiently transferring thermal energy. Material selection for these systems must account for potential hydrogen embrittlement, high-temperature corrosion, and thermal cycling stresses.

Contamination issues further complicate recovery efforts. Off-gases typically contain particulate matter, including iron dust and other mineral contaminants that can foul heat exchangers, catalysts, and gas separation membranes. These contaminants reduce system efficiency and increase maintenance requirements, necessitating robust filtration systems that themselves must operate at elevated temperatures.

Pressure management presents another significant challenge. The pressure differentials throughout the DRI process must be carefully controlled to maintain process stability while enabling efficient gas recovery. Pressure drops across filtration and heat recovery systems must be minimized to reduce the energy required for gas recirculation, which directly impacts the overall energy balance of the process.

Hydrogen separation and purification represent perhaps the most technically demanding aspect of off-gas recovery. Current technologies, including Pressure Swing Adsorption (PSA), membrane separation, and cryogenic distillation, each have limitations when applied to the specific conditions of DRI off-gases. PSA systems struggle with the temperature and contaminant profiles, membrane systems face durability challenges in these harsh environments, and cryogenic approaches require significant energy inputs that may offset recovery benefits.

System integration challenges arise when attempting to incorporate off-gas recovery into existing DRI plant designs. The intermittent nature of some DRI operations creates fluctuating off-gas volumes and compositions, requiring recovery systems with sufficient flexibility to handle these variations while maintaining efficiency. Additionally, the physical space constraints in existing facilities often limit retrofit options for comprehensive recovery systems.

Economic barriers further complicate implementation, as the capital expenditure for advanced recovery systems must be justified through operational savings or regulatory compliance. The return on investment calculations must account for maintenance costs, system reliability, and the market value of recovered energy and gases.

Current Off-Gas Utilization Technologies

01 Energy balance optimization in hydrogen DRI processes

Energy balance optimization in hydrogen-based direct reduced iron (DRI) processes involves careful management of thermal energy throughout the system. This includes optimizing the reduction temperature, controlling heat input/output ratios, and implementing advanced thermal management systems. Efficient energy balance reduces overall energy consumption while maintaining the quality of the reduced iron product. These optimizations can significantly improve the economic viability of hydrogen DRI processes by minimizing energy costs while maximizing production efficiency.- Energy balance optimization in hydrogen DRI processes: Optimizing energy balance in hydrogen-based direct reduced iron processes involves careful management of thermal energy throughout the system. This includes precise control of reduction temperatures, efficient heat transfer between process stages, and minimizing energy losses. Advanced process control systems monitor and adjust operating parameters to maintain optimal energy efficiency while ensuring high-quality iron production. These optimizations significantly reduce the overall energy consumption of the DRI process while maintaining or improving product quality.

- Off-gas utilization and recycling strategies: Off-gases from hydrogen DRI processes contain valuable components that can be recovered and reused. These gases typically include unreacted hydrogen, carbon monoxide, and carbon dioxide. Advanced gas separation and purification technologies enable the recovery of hydrogen for recirculation back into the reduction process. Additionally, carbon-containing gases can be processed through reforming or water-gas shift reactions to produce additional hydrogen. This recycling approach significantly improves process efficiency, reduces fresh hydrogen requirements, and minimizes environmental impact through reduced emissions.

- Heat recovery systems and thermal integration: Heat recovery systems in hydrogen DRI processes capture and utilize thermal energy from various process streams that would otherwise be wasted. This includes recovering heat from hot reduced iron, exhaust gases, and cooling systems. Technologies such as heat exchangers, waste heat boilers, and regenerative heating systems transfer this thermal energy to other parts of the process. Thermal integration between different process units maximizes overall energy efficiency. Advanced heat recovery configurations can generate steam for power production or provide preheating for process gases, significantly reducing external energy requirements.

- Innovative reactor designs for improved energy efficiency: Novel reactor designs for hydrogen DRI processes focus on enhancing energy efficiency through improved heat transfer, gas-solid contact, and reaction kinetics. These include fluidized bed reactors, moving bed systems with optimized gas flow patterns, and multi-stage reduction configurations. Some designs incorporate internal heat recovery mechanisms or catalytic elements to accelerate reduction reactions at lower temperatures. Advanced refractory materials and insulation systems minimize heat losses from reactor walls. These innovative designs reduce energy consumption while improving productivity and iron quality.

- Integration of renewable energy sources and hydrogen production: Integration of renewable energy sources with hydrogen DRI processes creates more sustainable and environmentally friendly ironmaking. This approach uses green hydrogen produced via electrolysis powered by renewable electricity from solar, wind, or hydroelectric sources. Some systems incorporate variable operation capabilities to align with renewable energy availability. Energy storage technologies help manage intermittency issues. This integration significantly reduces carbon emissions compared to conventional ironmaking processes. Advanced process control systems optimize the balance between hydrogen production, storage, and utilization in the DRI process based on energy availability and production demands.

02 Off-gas utilization and recycling strategies

Off-gas utilization in hydrogen DRI processes involves capturing, treating, and recycling process gases to improve overall system efficiency. These strategies include hydrogen recovery from off-gases, carbon monoxide recycling, and integration of off-gas streams into other plant processes. Advanced gas cleaning technologies remove impurities before recycling, while pressure swing adsorption systems can separate valuable components. Effective off-gas management reduces emissions, lowers fresh hydrogen requirements, and creates additional value streams from what would otherwise be waste gases.Expand Specific Solutions03 Heat recovery systems and thermal integration

Heat recovery systems in hydrogen DRI processes capture and reuse thermal energy from various process streams, including hot reduced iron, exhaust gases, and cooling systems. Technologies such as heat exchangers, waste heat boilers, and regenerative heating systems transfer thermal energy between process stages. Advanced thermal integration connects the DRI process with other plant operations, creating a more efficient overall energy network. These systems significantly reduce energy consumption, lower operational costs, and decrease the carbon footprint of the DRI production process.Expand Specific Solutions04 Innovative reactor designs for improved efficiency

Innovative reactor designs for hydrogen DRI processes focus on enhancing reduction efficiency, improving gas-solid contact, and optimizing heat transfer. These designs include fluidized bed reactors, moving bed systems with optimized flow patterns, and multi-stage reduction chambers. Some advanced reactors incorporate internal heat recovery mechanisms and specialized gas distribution systems. These design improvements lead to faster reduction rates, more uniform product quality, lower energy consumption, and increased production capacity compared to conventional DRI reactors.Expand Specific Solutions05 Integration of renewable energy sources

Integration of renewable energy sources into hydrogen DRI processes involves coupling the production system with green hydrogen generation and renewable electricity. This includes direct connection to solar, wind or hydroelectric power for electrolysis units, thermal energy storage systems to manage intermittent renewable supply, and smart control systems that optimize process operation based on renewable energy availability. These integrations reduce fossil fuel dependence, lower carbon emissions, and align with decarbonization goals for the steel industry, though they require careful system design to manage the variability of renewable energy sources.Expand Specific Solutions

Leading Companies in Hydrogen Metallurgy

The hydrogen-based Direct Reduced Iron (DRI) with energy balance off-gas utilization and heat recovery technology is currently in a growth phase, with an estimated market size of $2-3 billion annually and expanding at 15-20% CAGR. The competitive landscape features established industrial gas companies (Air Liquide), energy majors (Shell), and steel manufacturers (HBIS Group, Baoshan Iron & Steel) driving innovation. Technology maturity varies across players: Midrex Technologies leads with commercial-scale implementations, while companies like Toshiba Energy Systems and CISDI Engineering are advancing pilot projects. Research institutions (University of Science & Technology Beijing, Institute of Process Engineering CAS) are developing next-generation solutions focusing on efficiency improvements and carbon reduction, indicating the technology is transitioning from early adoption to mainstream implementation in decarbonization strategies.

Shell Oil Co.

Technical Solution: Shell has developed an innovative hydrogen energy integration system for DRI production that focuses on maximizing the circular use of process gases. Their technology employs a sophisticated pressure management approach that optimizes energy recovery from off-gases while maintaining process stability. The system features advanced catalytic reforming technology that can convert carbon-containing off-gases into additional hydrogen, creating a partially closed-loop system that reduces overall energy consumption. Shell's solution incorporates specialized heat recovery steam generators (HRSGs) designed to handle the unique composition of DRI off-gases, capturing thermal energy at multiple temperature points. Their process includes proprietary gas separation technology that selectively extracts hydrogen from mixed streams while minimizing energy penalties. The system also features advanced process control algorithms that continuously optimize the balance between hydrogen utilization, energy recovery, and production rate based on real-time monitoring of multiple process parameters.

Strengths: Extensive experience in large-scale hydrogen production and management; sophisticated process integration expertise; strong capabilities in process modeling and optimization. Weaknesses: Primary expertise in hydrocarbon processing rather than metallurgical applications; technology may require significant adaptation for different iron ore feedstocks; potentially higher implementation costs for smaller DRI facilities.

HBIS Group Co., Ltd.

Technical Solution: HBIS Group has developed a comprehensive energy management system for hydrogen-based DRI production that maximizes off-gas utilization through a multi-tiered approach. Their technology incorporates a cascading energy recovery system that extracts thermal energy at different temperature levels, matching heat sources with appropriate sinks throughout the production process. The system features specialized waste heat boilers that convert high-temperature off-gases into steam for power generation or process heating, achieving thermal recovery efficiencies of up to 75%. HBIS's solution also includes advanced gas cleaning technology that enables the separation of valuable components from off-gases while preserving their calorific value. Their process integrates with existing plant infrastructure through a modular design approach, allowing for phased implementation and optimization. The technology employs sophisticated digital twin modeling to continuously simulate and optimize energy flows, ensuring maximum recovery under varying production conditions.

Strengths: Extensive practical experience in steel production processes; integrated approach combining energy recovery with process optimization; strong focus on industrial implementation and operational reliability. Weaknesses: Technology still evolving for pure hydrogen-based reduction; potential challenges in retrofitting existing plants; requires significant process control expertise to maintain optimal performance.

Key Heat Recovery Innovations in DRI

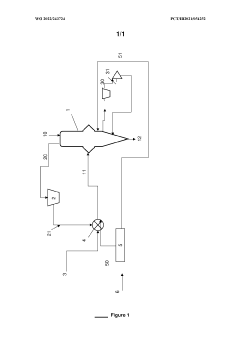

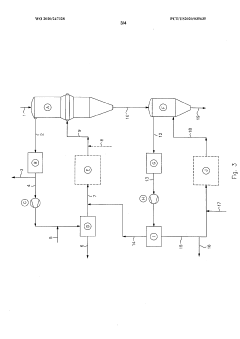

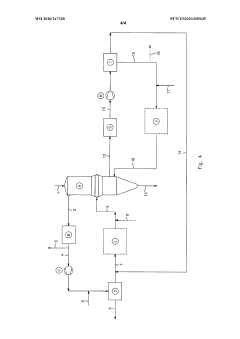

Method for manufacturing direct reduced iron and DRI manufacturing equipment

PatentWO2022243724A1

Innovation

- A method utilizing hydrogen extracted from coke oven gas, with the remaining coke oven gas being injected into the transition section of the DRI shaft to control the carbon content of the Direct Reduced Iron, and using CO2-neutral electricity for heating, to produce a CO2-neutral DRI with enhanced yield and reduced fossil energy use.

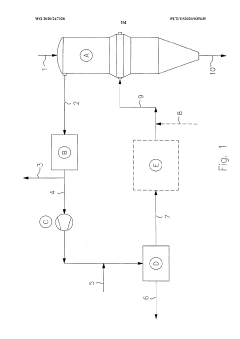

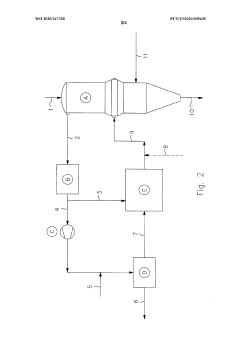

Direct reduction process utilizing hydrogen

PatentWO2020247328A1

Innovation

- The process integrates hydrogen production within the main gas loop using a solid oxide electrolyzer to recycle spent reducing gas, eliminating the need for externally supplied fuel and minimizing heat loss, while allowing for direct carbon control through carburizing gas injection, either within the shaft furnace or in a separate vessel.

Carbon Emission Reduction Potential

The implementation of hydrogen-based Direct Reduced Iron (DRI) technology presents significant carbon emission reduction potential compared to conventional blast furnace routes. When properly designed with energy balance optimization, off-gas utilization, and heat recovery systems, hydrogen DRI can achieve carbon emission reductions of 70-95% depending on the hydrogen source and process configuration.

Primary emission reductions come from replacing carbon-based reducing agents with hydrogen, eliminating the direct CO2 emissions associated with the reduction reaction. Conventional blast furnaces emit approximately 1.8-2.0 tonnes of CO2 per tonne of steel produced, while hydrogen DRI coupled with electric arc furnaces can potentially reduce this to 0.3-0.5 tonnes CO2 per tonne when using blue hydrogen, and below 0.1 tonnes when using green hydrogen.

Off-gas utilization represents a critical component of emission reduction strategies. Process gases containing unreacted hydrogen and other combustible components can be recycled back into the process, reducing fresh hydrogen requirements by 10-25%. This recycling not only improves resource efficiency but also prevents these gases from being flared or vented, avoiding additional emissions.

Heat recovery systems further enhance the carbon reduction potential by capturing thermal energy from various process streams. Advanced heat exchangers can recover up to 60% of waste heat from DRI shaft furnace off-gases, reducing the energy required for hydrogen preheating and other thermal processes. Each gigajoule of recovered heat potentially prevents 50-100 kg of CO2 emissions that would otherwise result from fossil fuel combustion to generate that energy.

The integration of hydrogen DRI with renewable energy sources compounds emission benefits. When green hydrogen produced via electrolysis powered by renewable electricity is used, the steel production becomes nearly carbon-neutral, with emissions primarily limited to upstream material production and transportation.

Life cycle assessments indicate that optimized hydrogen DRI facilities with comprehensive energy management systems can achieve carbon footprint reductions of up to 98% compared to traditional integrated steel mills. This represents one of the most promising decarbonization pathways for the steel industry, which currently accounts for approximately 7-9% of global CO2 emissions.

The scalability of these emission reductions depends on technological maturity, hydrogen availability, and economic factors. Current demonstration projects suggest that widespread adoption could reduce global steel industry emissions by 1.5-2.0 billion tonnes of CO2 annually by 2050, representing a significant contribution to global climate goals.

Primary emission reductions come from replacing carbon-based reducing agents with hydrogen, eliminating the direct CO2 emissions associated with the reduction reaction. Conventional blast furnaces emit approximately 1.8-2.0 tonnes of CO2 per tonne of steel produced, while hydrogen DRI coupled with electric arc furnaces can potentially reduce this to 0.3-0.5 tonnes CO2 per tonne when using blue hydrogen, and below 0.1 tonnes when using green hydrogen.

Off-gas utilization represents a critical component of emission reduction strategies. Process gases containing unreacted hydrogen and other combustible components can be recycled back into the process, reducing fresh hydrogen requirements by 10-25%. This recycling not only improves resource efficiency but also prevents these gases from being flared or vented, avoiding additional emissions.

Heat recovery systems further enhance the carbon reduction potential by capturing thermal energy from various process streams. Advanced heat exchangers can recover up to 60% of waste heat from DRI shaft furnace off-gases, reducing the energy required for hydrogen preheating and other thermal processes. Each gigajoule of recovered heat potentially prevents 50-100 kg of CO2 emissions that would otherwise result from fossil fuel combustion to generate that energy.

The integration of hydrogen DRI with renewable energy sources compounds emission benefits. When green hydrogen produced via electrolysis powered by renewable electricity is used, the steel production becomes nearly carbon-neutral, with emissions primarily limited to upstream material production and transportation.

Life cycle assessments indicate that optimized hydrogen DRI facilities with comprehensive energy management systems can achieve carbon footprint reductions of up to 98% compared to traditional integrated steel mills. This represents one of the most promising decarbonization pathways for the steel industry, which currently accounts for approximately 7-9% of global CO2 emissions.

The scalability of these emission reductions depends on technological maturity, hydrogen availability, and economic factors. Current demonstration projects suggest that widespread adoption could reduce global steel industry emissions by 1.5-2.0 billion tonnes of CO2 annually by 2050, representing a significant contribution to global climate goals.

Techno-Economic Assessment

The techno-economic assessment of energy balance off-gas utilization and heat recovery in hydrogen-based direct reduced iron (DRI) production reveals significant economic potential alongside environmental benefits. Initial capital expenditure for implementing comprehensive off-gas recovery systems ranges between $20-45 million for a standard DRI plant with 1-2 million tons annual capacity, depending on the sophistication of heat exchangers and energy conversion equipment deployed.

Operational cost savings present a compelling case for investment, with recovered energy potentially reducing external energy requirements by 15-25%. This translates to approximately $3-7 million in annual operational savings for medium-sized facilities, yielding payback periods typically between 3-7 years depending on energy prices and carbon taxation frameworks.

The levelized cost of steel production decreases by $5-15 per ton when efficient off-gas utilization systems are implemented, representing a 2-5% reduction in total production costs. This improvement in cost structure enhances competitiveness in increasingly price-sensitive global markets while simultaneously reducing carbon footprints.

Sensitivity analysis indicates that economic viability is most heavily influenced by three factors: natural gas prices, electricity costs, and carbon pricing mechanisms. With natural gas prices above $5/MMBtu, the economic case strengthens considerably. Similarly, in regions with electricity costs exceeding $0.08/kWh, the value proposition of self-generated power from recovered off-gases becomes particularly attractive.

Risk assessment identifies technological obsolescence and maintenance requirements as primary concerns. Advanced heat recovery systems typically require maintenance expenditures of 2-4% of capital costs annually, which must be factored into long-term financial planning. Additionally, the economic assessment must account for potential production disruptions during system installation, estimated at 5-10 days for major retrofits.

Comparative analysis with alternative technologies shows that off-gas recovery systems deliver superior returns compared to other decarbonization investments, with internal rates of return typically 3-5 percentage points higher than comparable green technologies in the steel sector. This favorable position is further enhanced when considering potential regulatory incentives for emissions reduction technologies.

The assessment concludes that facilities implementing comprehensive energy recovery systems can expect to reduce their carbon intensity by 0.15-0.30 tons CO₂ per ton of DRI produced, which at current and projected carbon prices represents an additional economic benefit of $4-12 per ton of production in markets with established carbon pricing mechanisms.

Operational cost savings present a compelling case for investment, with recovered energy potentially reducing external energy requirements by 15-25%. This translates to approximately $3-7 million in annual operational savings for medium-sized facilities, yielding payback periods typically between 3-7 years depending on energy prices and carbon taxation frameworks.

The levelized cost of steel production decreases by $5-15 per ton when efficient off-gas utilization systems are implemented, representing a 2-5% reduction in total production costs. This improvement in cost structure enhances competitiveness in increasingly price-sensitive global markets while simultaneously reducing carbon footprints.

Sensitivity analysis indicates that economic viability is most heavily influenced by three factors: natural gas prices, electricity costs, and carbon pricing mechanisms. With natural gas prices above $5/MMBtu, the economic case strengthens considerably. Similarly, in regions with electricity costs exceeding $0.08/kWh, the value proposition of self-generated power from recovered off-gases becomes particularly attractive.

Risk assessment identifies technological obsolescence and maintenance requirements as primary concerns. Advanced heat recovery systems typically require maintenance expenditures of 2-4% of capital costs annually, which must be factored into long-term financial planning. Additionally, the economic assessment must account for potential production disruptions during system installation, estimated at 5-10 days for major retrofits.

Comparative analysis with alternative technologies shows that off-gas recovery systems deliver superior returns compared to other decarbonization investments, with internal rates of return typically 3-5 percentage points higher than comparable green technologies in the steel sector. This favorable position is further enhanced when considering potential regulatory incentives for emissions reduction technologies.

The assessment concludes that facilities implementing comprehensive energy recovery systems can expect to reduce their carbon intensity by 0.15-0.30 tons CO₂ per ton of DRI produced, which at current and projected carbon prices represents an additional economic benefit of $4-12 per ton of production in markets with established carbon pricing mechanisms.

Unlock deeper insights with Patsnap Eureka Quick Research — get a full tech report to explore trends and direct your research. Try now!

Generate Your Research Report Instantly with AI Agent

Supercharge your innovation with Patsnap Eureka AI Agent Platform!