Carbon Capture Technologies Optimizing Energy Production

OCT 27, 20259 MIN READ

Generate Your Research Report Instantly with AI Agent

PatSnap Eureka helps you evaluate technical feasibility & market potential.

Carbon Capture Evolution and Objectives

Carbon capture technologies have evolved significantly over the past several decades, transitioning from theoretical concepts to practical applications in energy production systems. The journey began in the 1970s with initial research into carbon dioxide separation methods, primarily driven by enhanced oil recovery applications rather than environmental concerns. By the 1990s, as climate change awareness grew, carbon capture research expanded substantially, leading to the first industrial-scale projects in the early 2000s.

The evolution of carbon capture technologies has followed three distinct generations. First-generation technologies focused on post-combustion capture using amine-based solvents, which remain widely implemented despite their energy penalties. Second-generation approaches introduced pre-combustion capture and oxyfuel combustion, offering improved efficiency but requiring significant plant modifications. Current third-generation technologies explore novel materials like metal-organic frameworks, membrane systems, and direct air capture, promising reduced energy requirements and broader applicability.

The primary objective of carbon capture technologies in energy production is to enable continued use of fossil fuel resources while dramatically reducing greenhouse gas emissions. This balancing act aims to address the "energy trilemma" - providing secure, affordable, and environmentally sustainable energy. Specific technical objectives include reducing the energy penalty of capture processes below 10% (from current 20-30% levels), decreasing capital costs by at least 30%, and improving operational reliability for integration with variable renewable energy sources.

Another critical objective is developing versatile carbon capture solutions applicable across different energy production contexts, from natural gas combined cycle plants to coal-fired facilities and industrial processes like cement and steel manufacturing. This versatility is essential for widespread adoption across global energy systems with varying infrastructure characteristics and economic constraints.

Long-term objectives extend beyond mere capture to creating integrated carbon management systems that incorporate transportation infrastructure, utilization pathways, and permanent storage solutions. The ultimate goal is transforming carbon capture from a cost burden to a potential value stream through carbon utilization in products ranging from construction materials to synthetic fuels, thereby creating economic incentives that accelerate adoption while optimizing overall energy production efficiency.

The evolution of carbon capture technologies has followed three distinct generations. First-generation technologies focused on post-combustion capture using amine-based solvents, which remain widely implemented despite their energy penalties. Second-generation approaches introduced pre-combustion capture and oxyfuel combustion, offering improved efficiency but requiring significant plant modifications. Current third-generation technologies explore novel materials like metal-organic frameworks, membrane systems, and direct air capture, promising reduced energy requirements and broader applicability.

The primary objective of carbon capture technologies in energy production is to enable continued use of fossil fuel resources while dramatically reducing greenhouse gas emissions. This balancing act aims to address the "energy trilemma" - providing secure, affordable, and environmentally sustainable energy. Specific technical objectives include reducing the energy penalty of capture processes below 10% (from current 20-30% levels), decreasing capital costs by at least 30%, and improving operational reliability for integration with variable renewable energy sources.

Another critical objective is developing versatile carbon capture solutions applicable across different energy production contexts, from natural gas combined cycle plants to coal-fired facilities and industrial processes like cement and steel manufacturing. This versatility is essential for widespread adoption across global energy systems with varying infrastructure characteristics and economic constraints.

Long-term objectives extend beyond mere capture to creating integrated carbon management systems that incorporate transportation infrastructure, utilization pathways, and permanent storage solutions. The ultimate goal is transforming carbon capture from a cost burden to a potential value stream through carbon utilization in products ranging from construction materials to synthetic fuels, thereby creating economic incentives that accelerate adoption while optimizing overall energy production efficiency.

Market Analysis for Carbon Capture Solutions

The global carbon capture market is experiencing significant growth, driven by increasing environmental regulations and corporate sustainability commitments. As of 2023, the market was valued at approximately $7.5 billion, with projections indicating a compound annual growth rate (CAGR) of 19.2% through 2030, potentially reaching $35.9 billion by the end of the decade. This remarkable growth trajectory reflects the urgent need for decarbonization solutions across energy-intensive industries.

The demand for carbon capture technologies is particularly strong in power generation, oil and gas, cement manufacturing, and chemical production sectors. These industries collectively account for over 70% of global carbon emissions and represent the primary target markets for carbon capture solutions. The power generation sector alone constitutes about 40% of the current market share, as coal and natural gas plants seek to reduce their carbon footprint while maintaining operational viability.

Regional analysis reveals that North America currently leads the carbon capture market with approximately 35% market share, followed by Europe at 30% and Asia-Pacific at 25%. However, the Asia-Pacific region is expected to demonstrate the fastest growth rate in the coming years, driven by China's ambitious carbon neutrality goals and increasing industrial activity across developing economies in the region.

From a customer segmentation perspective, large industrial corporations and utility companies represent the primary adopters of carbon capture technologies, accounting for roughly 80% of market revenue. Government entities and research institutions constitute the remaining 20%, primarily focusing on pilot projects and technology development initiatives.

The economic viability of carbon capture solutions continues to improve, with the cost per ton of CO₂ captured decreasing from $80-120 in 2015 to $40-80 in 2023. This cost reduction trend is expected to continue as technologies mature and economies of scale are realized. Additionally, carbon pricing mechanisms and tax incentives in various regions are enhancing the financial attractiveness of these solutions.

Market barriers include high initial capital requirements, uncertain regulatory frameworks in some regions, and technical challenges related to storage and transportation infrastructure. Despite these challenges, investor interest remains robust, with venture capital and private equity investments in carbon capture startups exceeding $2.5 billion in 2022, a 150% increase from 2020 levels.

Customer adoption patterns indicate a preference for integrated solutions that combine capture, utilization, and storage capabilities, rather than standalone technologies. This trend is driving strategic partnerships between technology providers, infrastructure developers, and end-users to create comprehensive carbon management ecosystems.

The demand for carbon capture technologies is particularly strong in power generation, oil and gas, cement manufacturing, and chemical production sectors. These industries collectively account for over 70% of global carbon emissions and represent the primary target markets for carbon capture solutions. The power generation sector alone constitutes about 40% of the current market share, as coal and natural gas plants seek to reduce their carbon footprint while maintaining operational viability.

Regional analysis reveals that North America currently leads the carbon capture market with approximately 35% market share, followed by Europe at 30% and Asia-Pacific at 25%. However, the Asia-Pacific region is expected to demonstrate the fastest growth rate in the coming years, driven by China's ambitious carbon neutrality goals and increasing industrial activity across developing economies in the region.

From a customer segmentation perspective, large industrial corporations and utility companies represent the primary adopters of carbon capture technologies, accounting for roughly 80% of market revenue. Government entities and research institutions constitute the remaining 20%, primarily focusing on pilot projects and technology development initiatives.

The economic viability of carbon capture solutions continues to improve, with the cost per ton of CO₂ captured decreasing from $80-120 in 2015 to $40-80 in 2023. This cost reduction trend is expected to continue as technologies mature and economies of scale are realized. Additionally, carbon pricing mechanisms and tax incentives in various regions are enhancing the financial attractiveness of these solutions.

Market barriers include high initial capital requirements, uncertain regulatory frameworks in some regions, and technical challenges related to storage and transportation infrastructure. Despite these challenges, investor interest remains robust, with venture capital and private equity investments in carbon capture startups exceeding $2.5 billion in 2022, a 150% increase from 2020 levels.

Customer adoption patterns indicate a preference for integrated solutions that combine capture, utilization, and storage capabilities, rather than standalone technologies. This trend is driving strategic partnerships between technology providers, infrastructure developers, and end-users to create comprehensive carbon management ecosystems.

Global CCUS Technology Landscape and Barriers

Carbon capture, utilization, and storage (CCUS) technologies have evolved significantly over the past decades, yet their global implementation faces substantial barriers. Currently, the global CCUS landscape is characterized by uneven development across regions, with North America, Europe, and parts of Asia leading in both research and deployment. The United States, Canada, Norway, and Australia have established themselves as frontrunners, while China and Japan are rapidly accelerating their CCUS initiatives.

The technological landscape encompasses three primary capture approaches: post-combustion, pre-combustion, and oxy-fuel combustion. Post-combustion technologies, particularly amine-based solvent systems, dominate commercial applications due to their retrofit compatibility with existing infrastructure. However, these systems suffer from high energy penalties, typically consuming 15-30% of a power plant's output, significantly reducing overall efficiency.

Pre-combustion capture, integrated with gasification processes, offers higher CO2 concentration streams that facilitate more efficient capture but requires substantial modifications to existing plants. Oxy-fuel combustion, while promising higher capture rates, faces challenges related to the energy-intensive air separation process and materials durability under high-temperature oxygen-rich environments.

Critical barriers to widespread CCUS adoption include prohibitive costs, with current capture costs ranging from $40-120 per ton of CO2 depending on the source and technology. Transportation infrastructure limitations present another significant obstacle, as comprehensive CO2 pipeline networks remain underdeveloped in most regions. The geological storage capacity, while theoretically abundant, faces practical constraints related to site characterization, monitoring capabilities, and long-term liability concerns.

Regulatory frameworks governing CCUS vary dramatically across jurisdictions, creating uncertainty for potential investors. Many countries lack comprehensive policies addressing ownership rights for subsurface pore space, long-term liability frameworks, and monitoring requirements. This regulatory patchwork impedes cross-border projects and technology transfer.

Public perception and social acceptance represent underappreciated barriers, with concerns about safety, induced seismicity, and environmental justice issues affecting project development. Additionally, the energy penalty associated with capture processes remains a fundamental technical challenge, as current technologies require significant energy inputs that reduce the net climate benefit and economic viability of CCUS systems.

Integration challenges between capture technologies and host facilities further complicate implementation, particularly for retrofitting existing power plants and industrial facilities. The intermittent operation of renewable energy sources also creates technical complications for CCUS systems designed for steady-state operation, highlighting the need for more flexible capture technologies that can operate efficiently under variable conditions.

The technological landscape encompasses three primary capture approaches: post-combustion, pre-combustion, and oxy-fuel combustion. Post-combustion technologies, particularly amine-based solvent systems, dominate commercial applications due to their retrofit compatibility with existing infrastructure. However, these systems suffer from high energy penalties, typically consuming 15-30% of a power plant's output, significantly reducing overall efficiency.

Pre-combustion capture, integrated with gasification processes, offers higher CO2 concentration streams that facilitate more efficient capture but requires substantial modifications to existing plants. Oxy-fuel combustion, while promising higher capture rates, faces challenges related to the energy-intensive air separation process and materials durability under high-temperature oxygen-rich environments.

Critical barriers to widespread CCUS adoption include prohibitive costs, with current capture costs ranging from $40-120 per ton of CO2 depending on the source and technology. Transportation infrastructure limitations present another significant obstacle, as comprehensive CO2 pipeline networks remain underdeveloped in most regions. The geological storage capacity, while theoretically abundant, faces practical constraints related to site characterization, monitoring capabilities, and long-term liability concerns.

Regulatory frameworks governing CCUS vary dramatically across jurisdictions, creating uncertainty for potential investors. Many countries lack comprehensive policies addressing ownership rights for subsurface pore space, long-term liability frameworks, and monitoring requirements. This regulatory patchwork impedes cross-border projects and technology transfer.

Public perception and social acceptance represent underappreciated barriers, with concerns about safety, induced seismicity, and environmental justice issues affecting project development. Additionally, the energy penalty associated with capture processes remains a fundamental technical challenge, as current technologies require significant energy inputs that reduce the net climate benefit and economic viability of CCUS systems.

Integration challenges between capture technologies and host facilities further complicate implementation, particularly for retrofitting existing power plants and industrial facilities. The intermittent operation of renewable energy sources also creates technical complications for CCUS systems designed for steady-state operation, highlighting the need for more flexible capture technologies that can operate efficiently under variable conditions.

Current Carbon Capture Implementation Approaches

01 Absorption-based carbon capture optimization

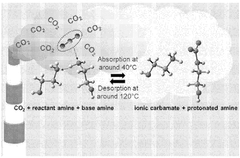

Optimization of absorption-based carbon capture technologies involves improving solvents, process parameters, and equipment design to enhance CO2 capture efficiency while reducing energy consumption. Advanced absorbents with higher CO2 selectivity and lower regeneration energy requirements are being developed. Process improvements include optimized absorption column designs, innovative heat integration strategies, and enhanced mass transfer mechanisms that maximize contact between flue gas and absorbent solutions.- Absorption-based carbon capture optimization: Optimization of absorption-based carbon capture technologies involves improving solvents, process parameters, and equipment design to enhance CO2 capture efficiency while reducing energy consumption. Advanced absorbents with higher CO2 selectivity and capacity, coupled with optimized process configurations such as heat integration and pressure swing systems, can significantly improve the overall performance of carbon capture systems. These technologies often incorporate real-time monitoring and control systems to maintain optimal operating conditions.

- Membrane technology for carbon capture: Membrane-based carbon capture technologies utilize selective permeable barriers to separate CO2 from gas mixtures. Optimization focuses on developing membranes with enhanced permeability, selectivity, and stability under various operating conditions. Advanced membrane materials, including mixed matrix membranes, facilitated transport membranes, and thermally rearranged polymers, offer improved performance characteristics. Process optimization includes multi-stage membrane configurations, hybrid systems combining membranes with other capture technologies, and integration with existing industrial processes to maximize efficiency.

- Adsorption-based carbon capture systems: Adsorption-based carbon capture technologies utilize solid sorbents to selectively capture CO2 from gas streams. Optimization involves developing advanced adsorbents with high CO2 selectivity, capacity, and regeneration efficiency. Process improvements include pressure/temperature swing adsorption cycles, vacuum swing adsorption, and electric swing adsorption. These systems can be optimized through computational modeling, process intensification, and integration with waste heat recovery to reduce energy penalties associated with sorbent regeneration.

- Biological and enzymatic carbon capture methods: Biological carbon capture technologies leverage natural processes such as photosynthesis and enzymatic reactions to capture and convert CO2. Optimization focuses on enhancing biological systems through genetic engineering of microorganisms, development of bioreactors with improved mass transfer characteristics, and immobilization of enzymes on various supports. These approaches can be integrated with industrial processes to capture CO2 directly from emission sources or from ambient air, with potential for converting captured carbon into valuable products through biocatalytic pathways.

- Direct air capture and mineralization technologies: Direct air capture (DAC) and mineralization technologies focus on extracting CO2 directly from ambient air or converting it into stable mineral forms. Optimization involves developing more energy-efficient DAC systems with improved sorbents and contactor designs to reduce the high energy requirements typically associated with low CO2 concentration in air. Mineralization processes are optimized by enhancing reaction kinetics, utilizing industrial waste materials as feedstocks, and developing continuous process systems that can operate at scale with minimal energy input and maximum conversion efficiency.

02 Adsorption and membrane technology enhancements

Carbon capture optimization through adsorption and membrane technologies focuses on developing novel materials with improved selectivity and capacity for CO2 separation. This includes engineered porous materials, metal-organic frameworks (MOFs), and advanced polymer membranes with enhanced permeability. Process innovations include pressure/temperature swing adsorption cycles, hybrid membrane systems, and multi-stage configurations that maximize separation efficiency while minimizing energy requirements and operational costs.Expand Specific Solutions03 Direct air capture (DAC) systems optimization

Optimization of direct air capture systems involves improving sorbent materials, energy efficiency, and process designs to extract CO2 directly from ambient air. Innovations include developing low-cost, durable sorbents with high CO2 selectivity, integrating renewable energy sources to power capture processes, and designing modular, scalable systems. Advanced heat management strategies and novel regeneration methods are being implemented to reduce the significant energy requirements associated with direct air capture.Expand Specific Solutions04 Biological and biomimetic carbon capture approaches

Biological and biomimetic approaches to carbon capture optimization leverage natural processes and structures for CO2 sequestration. These include engineered microalgae systems, artificial photosynthesis, enzyme-catalyzed capture mechanisms, and biomimetic materials that mimic natural carbon fixation processes. Innovations focus on enhancing growth rates, increasing carbon fixation efficiency, developing bioreactors with optimized light penetration and gas exchange, and creating sustainable systems that integrate with existing industrial processes.Expand Specific Solutions05 Integration and control systems for carbon capture

Optimization of carbon capture technologies through advanced integration and control systems involves developing sophisticated monitoring, automation, and process integration strategies. This includes AI-driven control algorithms that dynamically adjust operational parameters, smart sensors for real-time performance monitoring, and integrated systems that optimize energy use across capture facilities. Process integration innovations focus on heat recovery, waste utilization, and coupling carbon capture with utilization pathways to improve overall system efficiency and economic viability.Expand Specific Solutions

Leading CCUS Industry Players and Ecosystem

Carbon capture technologies in energy production are evolving rapidly, with the market currently in a growth phase. The global carbon capture market is projected to reach significant scale, driven by increasing environmental regulations and corporate sustainability goals. Technologically, solutions range from early-stage innovations to commercially deployed systems. Leading players demonstrate varying levels of maturity: established energy corporations like State Grid Corp. of China, Huaneng Clean Energy Research Institute, and Air Liquide SA have operational implementations, while research institutions such as Korea Institute of Energy Research, King Abdullah University, and Nanyang Technological University are advancing next-generation technologies. Specialized carbon capture firms like Aker Carbon Capture and NuScale Power are commercializing proprietary solutions, creating a competitive landscape that spans traditional energy players, research organizations, and technology-focused startups.

Huaneng Clean Energy Research Institute

Technical Solution: Huaneng Clean Energy Research Institute has pioneered the development of China's first large-scale carbon capture demonstration project at the Shidongkou No. 2 Power Plant in Shanghai, capturing approximately 120,000 tons of CO2 annually with a reported energy penalty of 14-18%. Their proprietary technology combines modified amine-based solvents with process optimizations specifically designed for high-sulfur coal power plants common in China. The institute has developed an integrated approach that addresses the unique challenges of capturing carbon from China's coal fleet, including innovations in flue gas pretreatment to handle higher particulate and sulfur content. Their second-generation technology, deployed at the Gaobeidian Power Plant in Beijing, achieved approximately 25% reduction in energy consumption compared to their first-generation system through advanced heat integration and solvent improvements. The institute has also developed novel solid sorbent technologies that show promise for reducing regeneration energy requirements by up to 30% compared to conventional liquid amine systems, with pilot testing underway at multiple facilities.

Strengths: Extensive experience with carbon capture in coal-fired power plants; technologies specifically optimized for China's energy infrastructure; demonstrated ability to scale solutions from laboratory to commercial implementation. Weaknesses: Technologies primarily focused on coal power applications with less development in other energy sectors; international deployment of their technologies has been limited compared to Western competitors.

Air Liquide SA

Technical Solution: Air Liquide has developed the Cryocap™ technology suite for carbon capture, which employs cryogenic separation processes to capture CO2 from industrial gas streams. Their flagship implementation at a hydrogen production facility in Port Jerome, France, demonstrates capture efficiency of approximately 90% while reducing overall energy consumption by up to 22% compared to conventional amine-based systems. The technology leverages Air Liquide's extensive expertise in gas separation and cryogenic processes, allowing for the simultaneous production of high-purity CO2 and increased hydrogen yields. For energy production applications, Air Liquide has adapted their technology to integrate with both pre-combustion and post-combustion processes, with particular success in hydrogen production facilities where the captured CO2 can be utilized for enhanced oil recovery or other industrial applications. The company has also developed specialized membrane-based separation technologies for natural gas processing that can simultaneously remove CO2 while optimizing methane recovery.

Strengths: Cryogenic approach offers lower energy penalties than many chemical absorption methods; technology produces high-purity CO2 suitable for direct utilization; significant operational experience across multiple industrial sectors. Weaknesses: Higher capital costs for cryogenic equipment compared to some competing technologies; process requires significant cooling energy which may limit application in certain geographical regions.

Key Carbon Capture Patents and Technical Innovations

Apparatuses and methods for carbon dioxide capturing and electrical energy producing system

PatentPendingCA3119677A1

Innovation

- An integrated and hybrid system that captures carbon dioxide from the atmosphere or flue gases while generating electrical energy internally, utilizing waste heat from hydrogen gas turbines and solid oxide fuel cells to increase the carbon dioxide absorption rate and reduce external power consumption, incorporating a tree-fashioned carbon dioxide capturing system and hybrid thermoelectric-generator and fuel cell units.

Systems and methods for combined carbon capture and thermal energy storage

PatentWO2025095856A1

Innovation

- A method and system for combined carbon capture and thermal energy storage, where CO2 is captured using a carbon capture medium that generates heat through an exothermic reaction, and this heat is utilized for thermal energy storage, with cooling applied to maintain the capture medium at a temperature below the CO2 regeneration temperature.

Policy Frameworks and Incentives for CCUS Adoption

The global policy landscape for Carbon Capture, Utilization, and Storage (CCUS) has evolved significantly over the past decade, with governments increasingly recognizing its critical role in achieving climate targets while maintaining energy security. Current policy frameworks can be categorized into three main approaches: direct subsidies, tax incentives, and regulatory mechanisms.

Direct subsidies have emerged as powerful catalysts for CCUS deployment, with the US Department of Energy's Carbon Capture Program providing over $4 billion in funding since 2010. Similarly, the EU Innovation Fund allocates substantial resources to demonstration projects, offering up to 60% of additional capital expenditure for breakthrough technologies. These subsidies significantly reduce the financial barriers to entry, particularly for first-of-a-kind commercial-scale projects.

Tax incentives represent another crucial policy tool, with the US Section 45Q tax credit standing as perhaps the most influential global example. The 2022 Inflation Reduction Act enhanced this mechanism, increasing credit values to $85 per metric ton for geological storage and $60 per ton for utilization or enhanced oil recovery. The UK's investment allowance for carbon storage and Norway's carbon tax exemptions for captured emissions demonstrate how tax policies can create economic viability for CCUS projects.

Regulatory frameworks provide the necessary legal certainty for long-term investments. The EU's CCS Directive establishes comprehensive guidelines for CO₂ storage site selection, monitoring requirements, and liability frameworks. Meanwhile, Australia's Offshore Petroleum and Greenhouse Gas Storage Act creates a title system for greenhouse gas injection and storage, addressing critical liability concerns that often deter private investment.

Carbon pricing mechanisms increasingly complement these policies, with systems in the EU, UK, and Canada creating economic incentives for emissions reduction. When carbon prices exceed the marginal cost of capture, CCUS becomes economically competitive without additional support. However, current carbon prices in most jurisdictions remain insufficient to drive widespread adoption without supplementary incentives.

International collaboration frameworks, such as the Clean Energy Ministerial's CCUS Initiative and Mission Innovation, facilitate knowledge sharing and coordinate research efforts across borders. These platforms help harmonize technical standards and regulatory approaches, reducing barriers to technology transfer and accelerating global deployment.

The effectiveness of these policy frameworks varies significantly across regions, with the most successful examples featuring complementary combinations of financial incentives, regulatory certainty, and carbon pricing. Future policy development must address the full value chain of CCUS technologies while balancing immediate deployment needs with long-term innovation support.

Direct subsidies have emerged as powerful catalysts for CCUS deployment, with the US Department of Energy's Carbon Capture Program providing over $4 billion in funding since 2010. Similarly, the EU Innovation Fund allocates substantial resources to demonstration projects, offering up to 60% of additional capital expenditure for breakthrough technologies. These subsidies significantly reduce the financial barriers to entry, particularly for first-of-a-kind commercial-scale projects.

Tax incentives represent another crucial policy tool, with the US Section 45Q tax credit standing as perhaps the most influential global example. The 2022 Inflation Reduction Act enhanced this mechanism, increasing credit values to $85 per metric ton for geological storage and $60 per ton for utilization or enhanced oil recovery. The UK's investment allowance for carbon storage and Norway's carbon tax exemptions for captured emissions demonstrate how tax policies can create economic viability for CCUS projects.

Regulatory frameworks provide the necessary legal certainty for long-term investments. The EU's CCS Directive establishes comprehensive guidelines for CO₂ storage site selection, monitoring requirements, and liability frameworks. Meanwhile, Australia's Offshore Petroleum and Greenhouse Gas Storage Act creates a title system for greenhouse gas injection and storage, addressing critical liability concerns that often deter private investment.

Carbon pricing mechanisms increasingly complement these policies, with systems in the EU, UK, and Canada creating economic incentives for emissions reduction. When carbon prices exceed the marginal cost of capture, CCUS becomes economically competitive without additional support. However, current carbon prices in most jurisdictions remain insufficient to drive widespread adoption without supplementary incentives.

International collaboration frameworks, such as the Clean Energy Ministerial's CCUS Initiative and Mission Innovation, facilitate knowledge sharing and coordinate research efforts across borders. These platforms help harmonize technical standards and regulatory approaches, reducing barriers to technology transfer and accelerating global deployment.

The effectiveness of these policy frameworks varies significantly across regions, with the most successful examples featuring complementary combinations of financial incentives, regulatory certainty, and carbon pricing. Future policy development must address the full value chain of CCUS technologies while balancing immediate deployment needs with long-term innovation support.

Economic Viability and Cost Reduction Strategies

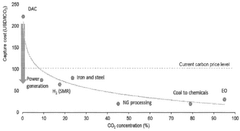

The economic viability of carbon capture technologies remains a critical challenge for widespread adoption in energy production systems. Current cost estimates for carbon capture range from $40 to $120 per ton of CO2 captured, depending on the technology and implementation context. These high costs create significant barriers to commercial deployment, particularly when compared to the market price of carbon in many jurisdictions, which often falls below these capture costs.

Cost reduction strategies are emerging across multiple fronts to address this economic gap. Process optimization represents a primary approach, with innovations in solvent chemistry reducing regeneration energy requirements by up to 30% in post-combustion capture systems. Advanced materials development, particularly in membrane and sorbent technologies, has demonstrated potential cost reductions of 15-25% through improved selectivity and durability characteristics.

Scale economies present another significant opportunity, with modeling studies indicating that increasing plant capacity from demonstration to commercial scale could reduce unit costs by 20-40%. This scaling effect is particularly pronounced for direct air capture technologies, where current costs exceed $600 per ton but show steep cost reduction potential with increased deployment volumes.

Integration strategies that combine carbon capture with existing industrial processes offer substantial economic benefits. Waste heat utilization from power generation or industrial operations can reduce the parasitic energy demands of carbon capture by 10-15%, directly improving economic performance. Additionally, revenue diversification through CO2 utilization pathways creates value streams that offset capture costs, with enhanced oil recovery currently providing $25-45 per ton of CO2 in certain markets.

Policy mechanisms remain essential for bridging remaining cost gaps. Tax incentives like the 45Q credit in the United States, which provides up to $50 per ton for geologic storage, significantly improve project economics. Carbon pricing mechanisms, particularly in regions with prices exceeding €50 per ton, create direct financial incentives for capture implementation. Public-private partnerships focused on shared infrastructure development, especially CO2 transport networks, distribute capital costs across multiple stakeholders and reduce individual project burdens.

Future cost trajectories appear promising, with learning curve analyses suggesting that carbon capture costs could decline by 10-12% for each doubling of installed capacity. This indicates potential for costs below $40 per ton by 2030-2035 with sustained deployment growth, approaching levels where market mechanisms could drive adoption without significant policy support.

Cost reduction strategies are emerging across multiple fronts to address this economic gap. Process optimization represents a primary approach, with innovations in solvent chemistry reducing regeneration energy requirements by up to 30% in post-combustion capture systems. Advanced materials development, particularly in membrane and sorbent technologies, has demonstrated potential cost reductions of 15-25% through improved selectivity and durability characteristics.

Scale economies present another significant opportunity, with modeling studies indicating that increasing plant capacity from demonstration to commercial scale could reduce unit costs by 20-40%. This scaling effect is particularly pronounced for direct air capture technologies, where current costs exceed $600 per ton but show steep cost reduction potential with increased deployment volumes.

Integration strategies that combine carbon capture with existing industrial processes offer substantial economic benefits. Waste heat utilization from power generation or industrial operations can reduce the parasitic energy demands of carbon capture by 10-15%, directly improving economic performance. Additionally, revenue diversification through CO2 utilization pathways creates value streams that offset capture costs, with enhanced oil recovery currently providing $25-45 per ton of CO2 in certain markets.

Policy mechanisms remain essential for bridging remaining cost gaps. Tax incentives like the 45Q credit in the United States, which provides up to $50 per ton for geologic storage, significantly improve project economics. Carbon pricing mechanisms, particularly in regions with prices exceeding €50 per ton, create direct financial incentives for capture implementation. Public-private partnerships focused on shared infrastructure development, especially CO2 transport networks, distribute capital costs across multiple stakeholders and reduce individual project burdens.

Future cost trajectories appear promising, with learning curve analyses suggesting that carbon capture costs could decline by 10-12% for each doubling of installed capacity. This indicates potential for costs below $40 per ton by 2030-2035 with sustained deployment growth, approaching levels where market mechanisms could drive adoption without significant policy support.

Unlock deeper insights with PatSnap Eureka Quick Research — get a full tech report to explore trends and direct your research. Try now!

Generate Your Research Report Instantly with AI Agent

Supercharge your innovation with PatSnap Eureka AI Agent Platform!