Carbon-negative Concrete: Challenges in Mass Production

OCT 1, 20259 MIN READ

Generate Your Research Report Instantly with AI Agent

Patsnap Eureka helps you evaluate technical feasibility & market potential.

Carbon-negative Concrete Background and Objectives

Concrete, as one of the most widely used construction materials globally, has long been associated with significant carbon emissions. Traditional concrete production accounts for approximately 8% of global CO2 emissions, primarily due to the energy-intensive process of cement manufacturing. Carbon-negative concrete represents a paradigm shift in construction materials, designed not only to reduce emissions but to actively sequester carbon dioxide throughout its lifecycle.

The evolution of concrete technology has progressed from conventional high-emission formulations to low-carbon alternatives, and now to carbon-negative solutions. This technological progression aligns with increasing global pressure to address climate change and achieve carbon neutrality targets set by international agreements such as the Paris Climate Accord and various national net-zero commitments.

Carbon-negative concrete utilizes alternative cementitious materials, carbon capture technologies, and innovative production processes to achieve a negative carbon footprint. These technologies include the incorporation of industrial byproducts like fly ash and slag, the use of novel binders such as geopolymers, and the integration of carbon sequestration mechanisms directly into the concrete matrix.

The primary objective of carbon-negative concrete development is to transform a major source of global emissions into a carbon sink while maintaining or enhancing the performance characteristics required for structural applications. This includes achieving comparable strength, durability, and workability to conventional concrete, ensuring regulatory compliance, and meeting industry standards for safety and reliability.

Current research and development efforts focus on scaling laboratory successes to industrial production levels, addressing challenges in raw material sourcing, process optimization, and quality control. The technical goals include reducing production costs to competitive levels, standardizing manufacturing protocols, and developing robust supply chains for alternative materials.

The trajectory of carbon-negative concrete technology indicates a potential inflection point in the construction industry, where sustainable building materials could become mainstream rather than niche alternatives. This transition is supported by growing regulatory pressures, increasing carbon pricing mechanisms, and shifting consumer preferences toward environmentally responsible construction practices.

The ultimate aim is to establish carbon-negative concrete as a commercially viable, widely adopted construction material that contributes significantly to global decarbonization efforts while meeting the growing infrastructure needs of an urbanizing world. This represents not only a technical challenge but an opportunity to fundamentally reimagine one of humanity's most essential building materials for a carbon-constrained future.

The evolution of concrete technology has progressed from conventional high-emission formulations to low-carbon alternatives, and now to carbon-negative solutions. This technological progression aligns with increasing global pressure to address climate change and achieve carbon neutrality targets set by international agreements such as the Paris Climate Accord and various national net-zero commitments.

Carbon-negative concrete utilizes alternative cementitious materials, carbon capture technologies, and innovative production processes to achieve a negative carbon footprint. These technologies include the incorporation of industrial byproducts like fly ash and slag, the use of novel binders such as geopolymers, and the integration of carbon sequestration mechanisms directly into the concrete matrix.

The primary objective of carbon-negative concrete development is to transform a major source of global emissions into a carbon sink while maintaining or enhancing the performance characteristics required for structural applications. This includes achieving comparable strength, durability, and workability to conventional concrete, ensuring regulatory compliance, and meeting industry standards for safety and reliability.

Current research and development efforts focus on scaling laboratory successes to industrial production levels, addressing challenges in raw material sourcing, process optimization, and quality control. The technical goals include reducing production costs to competitive levels, standardizing manufacturing protocols, and developing robust supply chains for alternative materials.

The trajectory of carbon-negative concrete technology indicates a potential inflection point in the construction industry, where sustainable building materials could become mainstream rather than niche alternatives. This transition is supported by growing regulatory pressures, increasing carbon pricing mechanisms, and shifting consumer preferences toward environmentally responsible construction practices.

The ultimate aim is to establish carbon-negative concrete as a commercially viable, widely adopted construction material that contributes significantly to global decarbonization efforts while meeting the growing infrastructure needs of an urbanizing world. This represents not only a technical challenge but an opportunity to fundamentally reimagine one of humanity's most essential building materials for a carbon-constrained future.

Market Analysis for Sustainable Construction Materials

The sustainable construction materials market is experiencing unprecedented growth, driven by increasing environmental concerns and regulatory pressures to reduce carbon emissions in the building sector. Currently valued at approximately $299 billion globally, this market is projected to reach $641 billion by 2030, with a compound annual growth rate of 11.4% between 2023 and 2030. Carbon-negative concrete represents one of the most promising segments within this expanding market.

Demand for carbon-negative concrete is primarily fueled by the construction industry's significant carbon footprint, which accounts for nearly 40% of global CO2 emissions, with traditional concrete production alone responsible for 8% of worldwide carbon emissions. This environmental impact has created urgent market pressure for alternative solutions that can maintain structural performance while reducing environmental harm.

Regional analysis reveals varying adoption rates and market potential. Europe leads in sustainable construction material implementation due to stringent regulations like the European Green Deal and the EU Taxonomy for Sustainable Activities. North America follows closely, with the United States investing heavily in green infrastructure projects. The Asia-Pacific region, despite being the largest concrete consumer globally, shows uneven adoption of carbon-negative alternatives, though China's recent environmental commitments signal potential for rapid market expansion.

Customer segmentation within this market reveals three primary buyer categories: government and public infrastructure projects, commercial developers pursuing green building certifications, and residential construction firms responding to consumer demand for sustainable housing options. Government procurement policies increasingly favor carbon-negative materials, creating a stable demand foundation for these products.

Pricing analysis indicates that carbon-negative concrete currently commands a premium of 15-30% over traditional concrete, presenting a significant barrier to mass adoption. However, this price differential is narrowing as production scales up and technologies mature. Market forecasts suggest price parity could be achieved within 5-7 years in developed markets.

Competitive landscape assessment shows established construction material giants like LafargeHolcim and HeidelbergCement investing heavily in carbon-negative concrete technologies, while innovative startups such as CarbonCure, Carbicrete, and Solidia are disrupting the market with novel approaches to carbon sequestration in concrete production. This dynamic competition is accelerating innovation and driving down costs.

Market barriers include conservative industry practices, limited awareness of carbon-negative concrete benefits, and concerns about long-term performance. However, these barriers are gradually eroding as successful demonstration projects accumulate and regulatory frameworks increasingly incentivize or mandate low-carbon building materials.

Demand for carbon-negative concrete is primarily fueled by the construction industry's significant carbon footprint, which accounts for nearly 40% of global CO2 emissions, with traditional concrete production alone responsible for 8% of worldwide carbon emissions. This environmental impact has created urgent market pressure for alternative solutions that can maintain structural performance while reducing environmental harm.

Regional analysis reveals varying adoption rates and market potential. Europe leads in sustainable construction material implementation due to stringent regulations like the European Green Deal and the EU Taxonomy for Sustainable Activities. North America follows closely, with the United States investing heavily in green infrastructure projects. The Asia-Pacific region, despite being the largest concrete consumer globally, shows uneven adoption of carbon-negative alternatives, though China's recent environmental commitments signal potential for rapid market expansion.

Customer segmentation within this market reveals three primary buyer categories: government and public infrastructure projects, commercial developers pursuing green building certifications, and residential construction firms responding to consumer demand for sustainable housing options. Government procurement policies increasingly favor carbon-negative materials, creating a stable demand foundation for these products.

Pricing analysis indicates that carbon-negative concrete currently commands a premium of 15-30% over traditional concrete, presenting a significant barrier to mass adoption. However, this price differential is narrowing as production scales up and technologies mature. Market forecasts suggest price parity could be achieved within 5-7 years in developed markets.

Competitive landscape assessment shows established construction material giants like LafargeHolcim and HeidelbergCement investing heavily in carbon-negative concrete technologies, while innovative startups such as CarbonCure, Carbicrete, and Solidia are disrupting the market with novel approaches to carbon sequestration in concrete production. This dynamic competition is accelerating innovation and driving down costs.

Market barriers include conservative industry practices, limited awareness of carbon-negative concrete benefits, and concerns about long-term performance. However, these barriers are gradually eroding as successful demonstration projects accumulate and regulatory frameworks increasingly incentivize or mandate low-carbon building materials.

Technical Barriers in Carbon-negative Concrete Production

The production of carbon-negative concrete faces several significant technical barriers that currently limit its widespread adoption and mass production capabilities. These challenges span across material science, manufacturing processes, and quality control domains.

The primary technical obstacle involves the carbon capture and utilization mechanisms within concrete production. Current carbon sequestration technologies require precise control of reaction conditions, including temperature, pressure, and catalyst presence, which are difficult to maintain consistently in large-scale production environments. The carbonation process, essential for carbon absorption, often occurs too slowly for commercial viability or requires energy-intensive acceleration methods that offset carbon benefits.

Material composition presents another substantial challenge. Carbon-negative concrete typically requires alternative cementitious materials such as calcined clays, fly ash, or slag, which exhibit variable chemical compositions depending on their source. This variability creates inconsistencies in final product performance, making quality control exceptionally difficult during mass production. Additionally, these alternative materials often demonstrate different hydration kinetics compared to traditional Portland cement, necessitating modified curing protocols that are challenging to implement at scale.

Process integration barriers also significantly impede mass production efforts. Retrofitting existing concrete manufacturing facilities to accommodate carbon-negative production methods requires substantial capital investment and technical modifications. The integration of carbon capture equipment with traditional concrete batching plants presents complex engineering challenges related to space constraints, process flow disruptions, and safety considerations.

Quality assurance represents a critical technical hurdle. Current testing standards and certification protocols are primarily designed for conventional concrete, creating regulatory uncertainties for carbon-negative alternatives. The long-term durability and performance characteristics of carbon-negative concrete remain inadequately documented, raising concerns among engineers and building code officials about structural integrity and service life predictions.

Energy requirements pose additional technical complications. While carbon-negative concrete aims to reduce overall emissions, certain production pathways actually require higher energy inputs for specialized processing steps like mineral carbonation or accelerated curing. This creates a technical paradox where carbon benefits may be partially offset by increased energy consumption unless renewable energy sources are integrated into the manufacturing process.

Supply chain limitations further constrain mass production capabilities. The specialized additives, catalysts, and alternative binders required for carbon-negative concrete formulations often have limited availability or face production bottlenecks of their own, creating material supply uncertainties that complicate large-scale manufacturing planning and implementation.

The primary technical obstacle involves the carbon capture and utilization mechanisms within concrete production. Current carbon sequestration technologies require precise control of reaction conditions, including temperature, pressure, and catalyst presence, which are difficult to maintain consistently in large-scale production environments. The carbonation process, essential for carbon absorption, often occurs too slowly for commercial viability or requires energy-intensive acceleration methods that offset carbon benefits.

Material composition presents another substantial challenge. Carbon-negative concrete typically requires alternative cementitious materials such as calcined clays, fly ash, or slag, which exhibit variable chemical compositions depending on their source. This variability creates inconsistencies in final product performance, making quality control exceptionally difficult during mass production. Additionally, these alternative materials often demonstrate different hydration kinetics compared to traditional Portland cement, necessitating modified curing protocols that are challenging to implement at scale.

Process integration barriers also significantly impede mass production efforts. Retrofitting existing concrete manufacturing facilities to accommodate carbon-negative production methods requires substantial capital investment and technical modifications. The integration of carbon capture equipment with traditional concrete batching plants presents complex engineering challenges related to space constraints, process flow disruptions, and safety considerations.

Quality assurance represents a critical technical hurdle. Current testing standards and certification protocols are primarily designed for conventional concrete, creating regulatory uncertainties for carbon-negative alternatives. The long-term durability and performance characteristics of carbon-negative concrete remain inadequately documented, raising concerns among engineers and building code officials about structural integrity and service life predictions.

Energy requirements pose additional technical complications. While carbon-negative concrete aims to reduce overall emissions, certain production pathways actually require higher energy inputs for specialized processing steps like mineral carbonation or accelerated curing. This creates a technical paradox where carbon benefits may be partially offset by increased energy consumption unless renewable energy sources are integrated into the manufacturing process.

Supply chain limitations further constrain mass production capabilities. The specialized additives, catalysts, and alternative binders required for carbon-negative concrete formulations often have limited availability or face production bottlenecks of their own, creating material supply uncertainties that complicate large-scale manufacturing planning and implementation.

Current Manufacturing Solutions and Processes

01 Carbon capture and sequestration in concrete production

Technologies that capture and store carbon dioxide during the concrete manufacturing process, effectively making the concrete carbon-negative. These methods involve injecting CO2 into concrete during curing, where it becomes permanently mineralized and transforms into calcium carbonate, enhancing the concrete's strength while reducing its carbon footprint.- Carbon capture and sequestration in concrete production: Technologies that capture carbon dioxide during or after concrete production, effectively sequestering CO2 in the concrete matrix. These methods involve chemical reactions that permanently bind carbon dioxide within the concrete, transforming a traditionally carbon-intensive material into one that can serve as a carbon sink. This approach helps reduce the overall carbon footprint of concrete while maintaining or even improving its structural properties.

- Alternative cementitious materials for carbon-negative concrete: Development of novel cement alternatives that inherently absorb more carbon dioxide than they emit during production. These materials include geopolymers, alkali-activated materials, and other binders that require less energy to produce than traditional Portland cement while having greater carbon absorption capacity. By replacing conventional cement with these alternatives, concrete can achieve carbon negativity over its lifecycle.

- Carbon mineralization processes in concrete: Methods that accelerate the natural carbonation process in concrete through enhanced mineralization techniques. These processes involve exposing concrete to concentrated carbon dioxide under controlled conditions, promoting the formation of stable carbonate minerals within the concrete matrix. This approach not only sequesters carbon but can also improve concrete durability and strength properties.

- Supplementary cementitious materials for carbon reduction: Incorporation of industrial byproducts and waste materials as supplementary cementitious materials to reduce the carbon footprint of concrete. Materials such as fly ash, slag, silica fume, and other pozzolanic materials can partially replace cement in concrete mixtures, reducing embodied carbon while utilizing materials that would otherwise be discarded. This approach creates a circular economy solution while contributing to carbon negativity.

- Carbon-negative concrete curing technologies: Specialized curing methods designed to maximize carbon dioxide uptake during the concrete hardening process. These technologies involve exposing fresh concrete to carbon dioxide-rich environments under optimized temperature, pressure, and humidity conditions. By integrating carbon capture directly into the manufacturing process, these methods can transform concrete production from a carbon source to a carbon sink.

02 Alternative cementitious materials for carbon reduction

Use of alternative materials to replace traditional Portland cement, which is responsible for significant carbon emissions. These alternatives include geopolymers, alkali-activated materials, and supplementary cementitious materials like fly ash, slag, and natural pozzolans that require less energy to produce and can absorb CO2 during their lifecycle, contributing to carbon negativity.Expand Specific Solutions03 Biomass incorporation in concrete formulations

Integration of biomass materials such as agricultural waste, wood products, or algae into concrete mixtures. These bio-based additives store carbon captured during their growth phase and can replace carbon-intensive components while potentially improving certain concrete properties like thermal insulation and weight reduction.Expand Specific Solutions04 Enhanced carbonation techniques for concrete

Accelerated carbonation processes that promote the absorption of atmospheric CO2 by concrete throughout its lifecycle. These techniques involve specialized curing conditions, surface treatments, or the addition of catalysts that increase the rate and extent of carbonation, allowing concrete structures to serve as carbon sinks over time.Expand Specific Solutions05 Carbon-negative concrete lifecycle management systems

Comprehensive approaches to concrete production, use, and end-of-life management that result in net carbon sequestration. These systems combine multiple carbon reduction strategies with monitoring technologies to track carbon balance throughout the concrete lifecycle, including recycling processes that further enhance carbon uptake in secondary concrete products.Expand Specific Solutions

Leading Companies and Research Institutions

The carbon-negative concrete market is in its early growth phase, characterized by significant R&D investment but limited commercial-scale implementation. Market size is projected to expand rapidly as construction industries face increasing pressure to reduce carbon footprints, with estimates suggesting a multi-billion dollar opportunity by 2030. Technical challenges persist in scaling production while maintaining performance and cost-competitiveness. Leading players demonstrate varying levels of technological maturity: Solidia Technologies has advanced commercialization of CO2-curing processes, while Calera Corporation focuses on carbon mineralization. Academic institutions like Southeast University and Shandong University contribute fundamental research, while industrial giants including Saudi Aramco and Huaxin Cement leverage their infrastructure to develop implementation pathways. Smaller innovators such as Materr'Up and Clear Zero Carbon are introducing novel approaches, though widespread adoption remains constrained by regulatory frameworks and production economics.

Solidia Technologies, Inc.

Technical Solution: Solidia Technologies has pioneered a low-carbon cement and concrete production system that reduces CO2 emissions by up to 70% compared to traditional Portland cement. Their approach involves two key innovations: (1) a modified cement formulation that requires lower kiln temperatures during production (reducing energy consumption by 30-40%), and (2) a CO2-based curing process that replaces water curing in traditional concrete manufacturing. The Solidia Cement™ is produced using the same raw materials and equipment as traditional cement but with a different formulation that creates calcium silicate phases that readily react with CO2. During the concrete curing process, CO2 is injected and chemically reacts with the cement to form calcium carbonate, permanently sequestering the carbon. This process not only reduces emissions but actually consumes CO2, making it potentially carbon-negative when renewable energy is used in production. Solidia's technology has been validated through partnerships with major industry players like LafargeHolcim and has been implemented in commercial precast concrete applications.

Strengths: Significantly lower carbon footprint; uses existing manufacturing infrastructure; faster curing time (24 hours vs. 28 days for traditional concrete); reduced water usage by up to 80%; improved concrete performance characteristics including strength and durability. Weaknesses: Currently limited to precast applications; requires pure CO2 source for curing; market adoption faces industry conservatism; higher initial costs compared to traditional methods; requires retraining of workforce.

Clear Zero Carbon (Beijing) Technology Co., Ltd.

Technical Solution: Clear Zero Carbon has developed a mineralization-based carbon capture and utilization technology specifically designed for the cement industry in China. Their approach involves capturing CO2 from cement kiln exhaust gases and converting it into calcium and magnesium carbonates through an accelerated mineralization process. These carbonates are then incorporated back into concrete production as supplementary cementitious materials or aggregates. The company's proprietary catalyst system significantly increases the carbonation reaction rate, making the process economically viable at industrial scale. Clear Zero Carbon's technology can be retrofitted to existing cement plants, capturing up to 30% of emissions directly from the production process. Additionally, they've developed a specialized concrete formulation that continues to absorb CO2 throughout its lifetime, enhancing the carbon-negative potential. The company has implemented this technology in several cement plants across northern China, demonstrating CO2 reduction of approximately 200kg per ton of cement produced. Their process also improves concrete durability by reducing porosity through the formation of stable carbonate minerals within the concrete matrix.

Strengths: Directly addresses emissions from existing cement plants; creates a circular carbon economy within cement production; improves concrete durability properties; relatively low implementation cost compared to other carbon capture technologies; aligned with China's carbon neutrality goals. Weaknesses: Currently achieves only partial carbon capture; requires consistent CO2 concentration in flue gas; energy requirements for the mineralization process; limited international deployment experience; regulatory hurdles for widespread adoption.

Key Patents and Scientific Breakthroughs

Controlling carbonation

PatentWO2021255340A1

Innovation

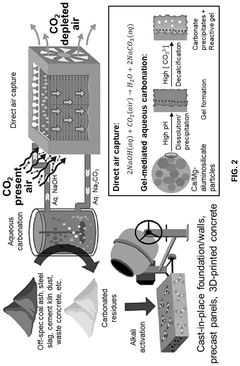

- A method for controlling carbonation by adjusting the total concentration of dissolved silicon and/or aluminium in a mix, which is cured with carbon dioxide, using an alkaline substance to activate the raw material, thereby increasing carbon dioxide uptake and reducing the need for cement in concrete production.

Cementitious materials and methods of making and using same

PatentPendingUS20250042811A1

Innovation

- A carbon mineralization-based direct-air capture process is used to produce carbon-negative cementitious materials by capturing CO2 from the air through an aqueous carbonation cycle, enhancing the pozzolanic reactivity of industrial mineral wastes, and incorporating the captured CO2 as solid carbonate in the concrete.

Environmental Impact Assessment

The environmental impact assessment of carbon-negative concrete reveals significant potential for reducing the construction industry's carbon footprint. Traditional concrete production accounts for approximately 8% of global CO2 emissions, primarily from cement manufacturing. Carbon-negative concrete technologies aim to reverse this trend by sequestering more carbon than is emitted during production.

Life cycle assessments indicate that carbon-negative concrete can achieve net carbon sequestration ranging from 50-300 kg CO2 per cubic meter, depending on the specific technology and implementation methods. This represents a dramatic improvement over conventional concrete, which typically emits 400-500 kg CO2 per cubic meter.

Water usage metrics show varied results across different carbon-negative formulations. Some technologies require additional water for carbonation processes, while others demonstrate reduced water requirements compared to traditional concrete. This variability necessitates region-specific implementation strategies, particularly in water-stressed areas.

Land use impacts must be carefully considered, especially regarding the sourcing of supplementary cementitious materials like fly ash, slag, and natural pozzolans. Sustainable sourcing practices are essential to prevent habitat disruption and biodiversity loss associated with raw material extraction.

Air quality improvements represent another significant benefit, as carbon-negative concrete production typically generates fewer particulate emissions than traditional cement kilns. However, the transportation of specialized materials may partially offset these gains if supply chains are not optimized for proximity.

Waste stream analysis reveals promising circular economy opportunities, as many carbon-negative concrete formulations incorporate industrial byproducts that would otherwise require disposal. This diverts materials from landfills while reducing the need for virgin resource extraction.

Energy consumption patterns differ substantially from conventional concrete production. While some carbon-negative processes require additional energy for specialized curing environments, others leverage ambient carbonation that requires minimal energy input. The net environmental benefit depends heavily on the energy sources powering these processes, highlighting the importance of renewable energy integration in production facilities.

Comprehensive environmental impact modeling suggests that scaling carbon-negative concrete to 10% of global concrete production could sequester approximately 0.5 gigatons of CO2 annually, representing a meaningful contribution to climate change mitigation efforts.

Life cycle assessments indicate that carbon-negative concrete can achieve net carbon sequestration ranging from 50-300 kg CO2 per cubic meter, depending on the specific technology and implementation methods. This represents a dramatic improvement over conventional concrete, which typically emits 400-500 kg CO2 per cubic meter.

Water usage metrics show varied results across different carbon-negative formulations. Some technologies require additional water for carbonation processes, while others demonstrate reduced water requirements compared to traditional concrete. This variability necessitates region-specific implementation strategies, particularly in water-stressed areas.

Land use impacts must be carefully considered, especially regarding the sourcing of supplementary cementitious materials like fly ash, slag, and natural pozzolans. Sustainable sourcing practices are essential to prevent habitat disruption and biodiversity loss associated with raw material extraction.

Air quality improvements represent another significant benefit, as carbon-negative concrete production typically generates fewer particulate emissions than traditional cement kilns. However, the transportation of specialized materials may partially offset these gains if supply chains are not optimized for proximity.

Waste stream analysis reveals promising circular economy opportunities, as many carbon-negative concrete formulations incorporate industrial byproducts that would otherwise require disposal. This diverts materials from landfills while reducing the need for virgin resource extraction.

Energy consumption patterns differ substantially from conventional concrete production. While some carbon-negative processes require additional energy for specialized curing environments, others leverage ambient carbonation that requires minimal energy input. The net environmental benefit depends heavily on the energy sources powering these processes, highlighting the importance of renewable energy integration in production facilities.

Comprehensive environmental impact modeling suggests that scaling carbon-negative concrete to 10% of global concrete production could sequester approximately 0.5 gigatons of CO2 annually, representing a meaningful contribution to climate change mitigation efforts.

Cost-Benefit Analysis and Scalability Challenges

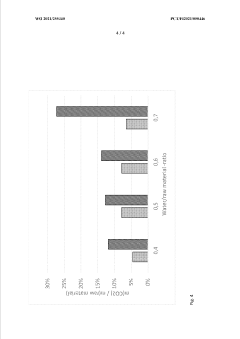

The economic viability of carbon-negative concrete faces significant challenges when transitioning from laboratory settings to industrial-scale production. Current cost analyses indicate that carbon-negative concrete variants are approximately 20-35% more expensive than traditional Portland cement concrete, primarily due to the specialized materials and processing requirements. This cost premium represents a substantial barrier to widespread adoption, particularly in price-sensitive construction markets where material decisions are often driven by immediate economic considerations rather than long-term environmental benefits.

When evaluating the cost-benefit equation, it's essential to consider both direct and indirect economic factors. Direct costs include raw materials, manufacturing processes, transportation, and installation. Carbon capture technologies integrated into concrete production add significant capital expenditure requirements, with current estimates suggesting payback periods of 7-10 years for most advanced systems. These extended return timelines often conflict with typical industry investment horizons of 3-5 years.

The scalability challenges are equally formidable from a technical perspective. Current carbon-negative concrete production methods that have demonstrated success in controlled environments face numerous obstacles when scaled to commercial volumes. Issues include maintaining consistent quality across large batches, ensuring uniform carbon sequestration rates, and adapting existing manufacturing infrastructure to accommodate new processes. Production capacity limitations represent another critical bottleneck, with most specialized facilities currently capable of producing only 10-15% of the volume needed to meet potential market demand.

Supply chain constraints further complicate scalability efforts. Many carbon-negative concrete formulations rely on specific industrial byproducts or specialized additives with limited availability. For instance, the supply of high-quality fly ash and slag, common supplementary cementitious materials in low-carbon concrete, is decreasing as coal power plants are decommissioned globally. This creates potential resource bottlenecks that could impede large-scale production.

Regulatory frameworks and certification processes present additional challenges to scaling production. The relatively novel nature of carbon-negative concrete means that building codes, standards, and certification processes are still evolving. This regulatory uncertainty increases risk for manufacturers and can slow adoption rates, as construction projects typically require materials with established performance records and regulatory approvals.

Despite these challenges, economic modeling suggests that economies of scale could eventually reduce the cost premium of carbon-negative concrete to 5-10% above conventional alternatives. This more modest differential, combined with potential carbon pricing mechanisms and regulatory incentives, could create viable pathways to commercial-scale production within the next decade.

When evaluating the cost-benefit equation, it's essential to consider both direct and indirect economic factors. Direct costs include raw materials, manufacturing processes, transportation, and installation. Carbon capture technologies integrated into concrete production add significant capital expenditure requirements, with current estimates suggesting payback periods of 7-10 years for most advanced systems. These extended return timelines often conflict with typical industry investment horizons of 3-5 years.

The scalability challenges are equally formidable from a technical perspective. Current carbon-negative concrete production methods that have demonstrated success in controlled environments face numerous obstacles when scaled to commercial volumes. Issues include maintaining consistent quality across large batches, ensuring uniform carbon sequestration rates, and adapting existing manufacturing infrastructure to accommodate new processes. Production capacity limitations represent another critical bottleneck, with most specialized facilities currently capable of producing only 10-15% of the volume needed to meet potential market demand.

Supply chain constraints further complicate scalability efforts. Many carbon-negative concrete formulations rely on specific industrial byproducts or specialized additives with limited availability. For instance, the supply of high-quality fly ash and slag, common supplementary cementitious materials in low-carbon concrete, is decreasing as coal power plants are decommissioned globally. This creates potential resource bottlenecks that could impede large-scale production.

Regulatory frameworks and certification processes present additional challenges to scaling production. The relatively novel nature of carbon-negative concrete means that building codes, standards, and certification processes are still evolving. This regulatory uncertainty increases risk for manufacturers and can slow adoption rates, as construction projects typically require materials with established performance records and regulatory approvals.

Despite these challenges, economic modeling suggests that economies of scale could eventually reduce the cost premium of carbon-negative concrete to 5-10% above conventional alternatives. This more modest differential, combined with potential carbon pricing mechanisms and regulatory incentives, could create viable pathways to commercial-scale production within the next decade.

Unlock deeper insights with Patsnap Eureka Quick Research — get a full tech report to explore trends and direct your research. Try now!

Generate Your Research Report Instantly with AI Agent

Supercharge your innovation with Patsnap Eureka AI Agent Platform!