System for financial risk management administration

a financial risk and management system technology, applied in the field of financial risk management administration, can solve the problems of unappealing risk involved over a long period of time before annuitization, unfavorable investment risk of annuity contract owner, and reduced death benefit to an insignificant amount, so as to increase or decrease the risk associated with annuity.

- Summary

- Abstract

- Description

- Claims

- Application Information

AI Technical Summary

Benefits of technology

Problems solved by technology

Method used

Image

Examples

Embodiment Construction

[0128]As required, a detailed illustrative embodiment of the present invention is disclosed herein. However, techniques, systems and operating structures in accordance with the present invention may be embodied in a wide variety of forms and modes, some of which may be quite different from those in the disclosed embodiment. Consequently, the specific structural and functional details disclosed herein are merely representative, yet in that regard, they are deemed to afford the best embodiment for purposes of disclosure and to provide a basis for the claims herein, which define the scope of the present invention. The following presents a detailed description of the preferred embodiment of the present invention.

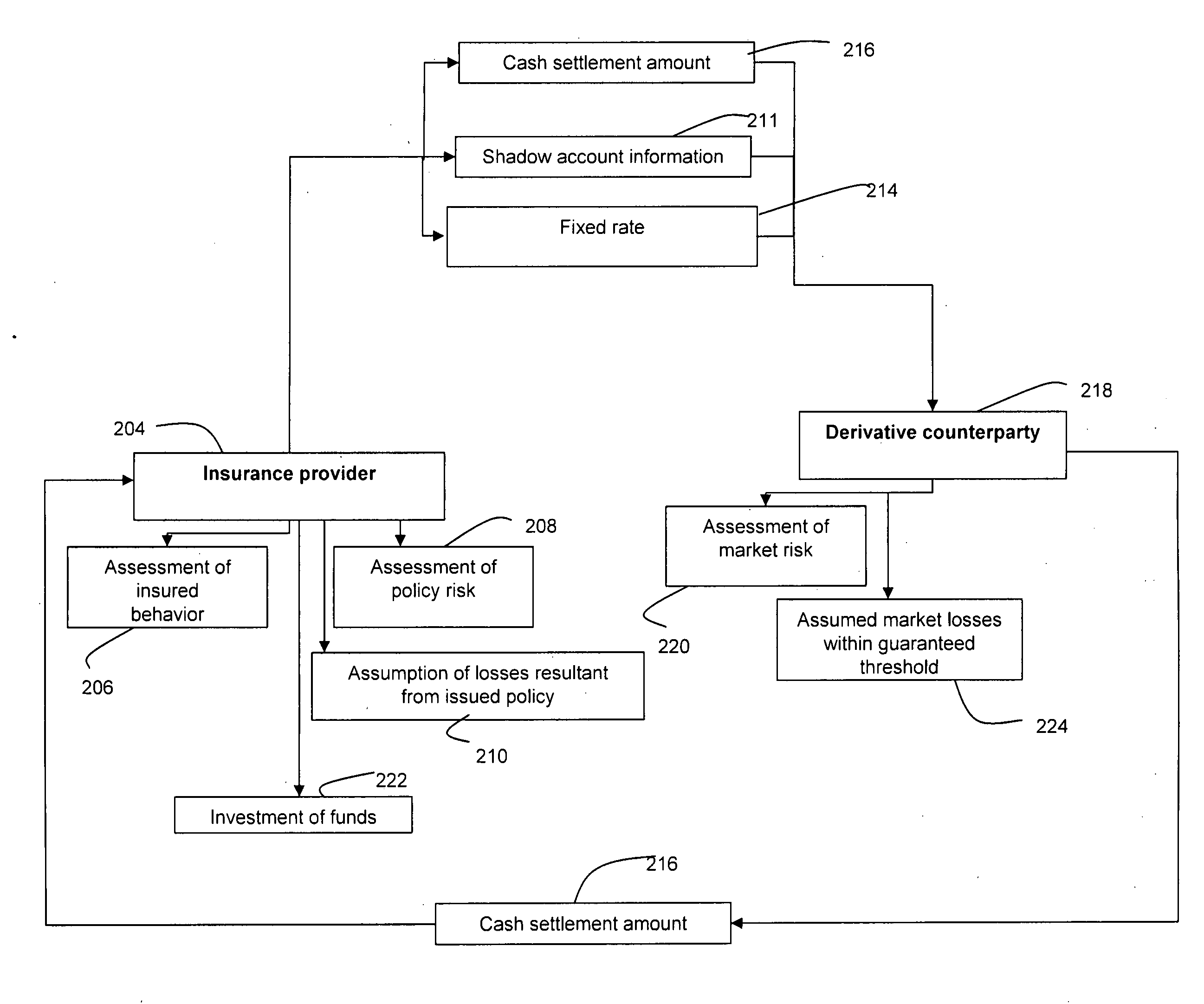

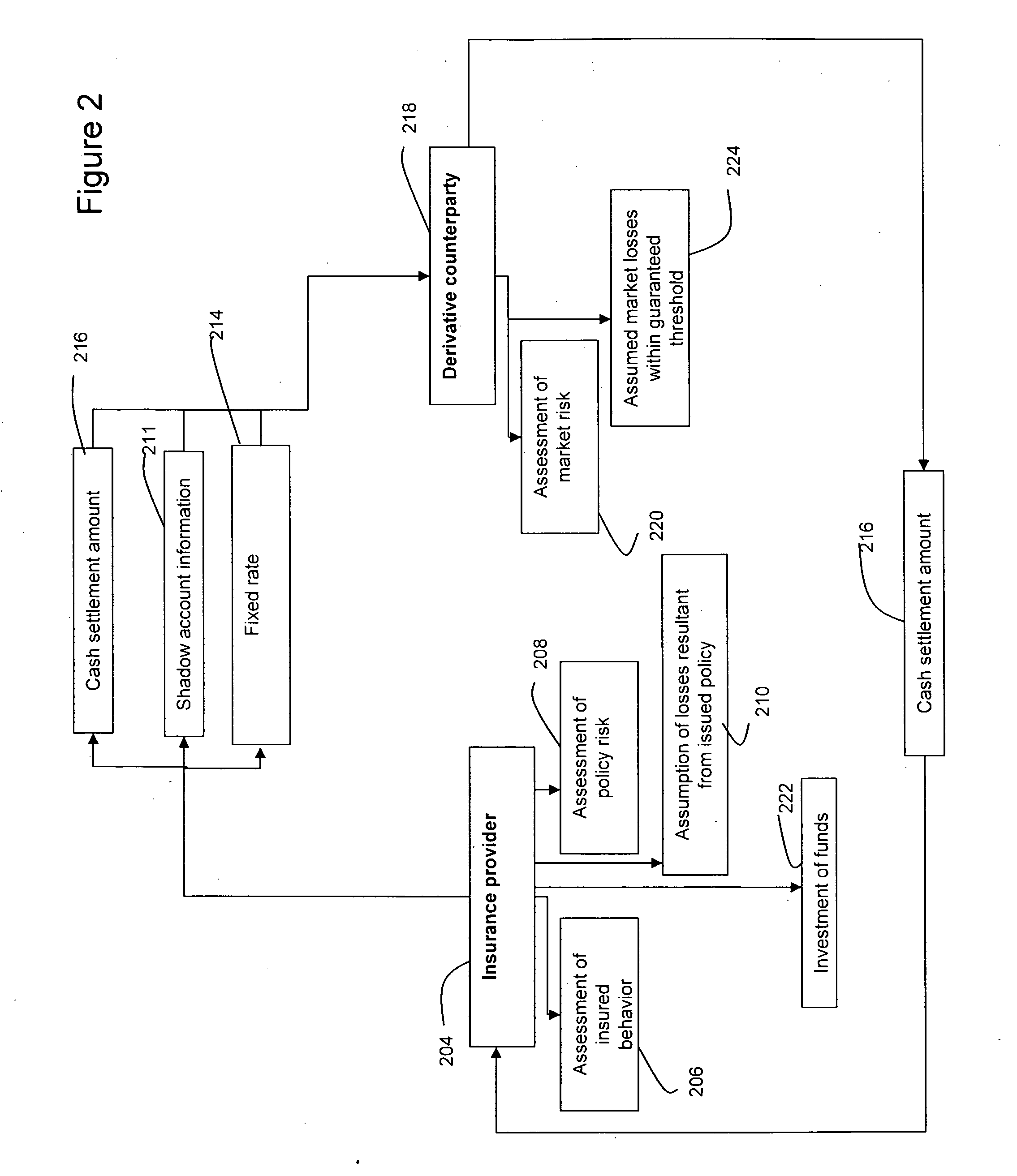

[0129]Among other factors, hedging effectiveness on VA guarantees using generic hedging instruments, known as “vanilla hedging instruments,” is dependent upon the size, frequency and correlation of movements in critical capital markets variables. Generally, small changes in valu...

PUM

Login to View More

Login to View More Abstract

Description

Claims

Application Information

Login to View More

Login to View More