VaR confidence interval prediction method

A technology of confidence interval and prediction method, which is applied in the field of risk measurement and can solve problems such as undiscussed sampling error VaR confidence interval

- Summary

- Abstract

- Description

- Claims

- Application Information

AI Technical Summary

Problems solved by technology

Method used

Image

Examples

Embodiment Construction

[0041] The present invention will be further described below in conjunction with specific examples.

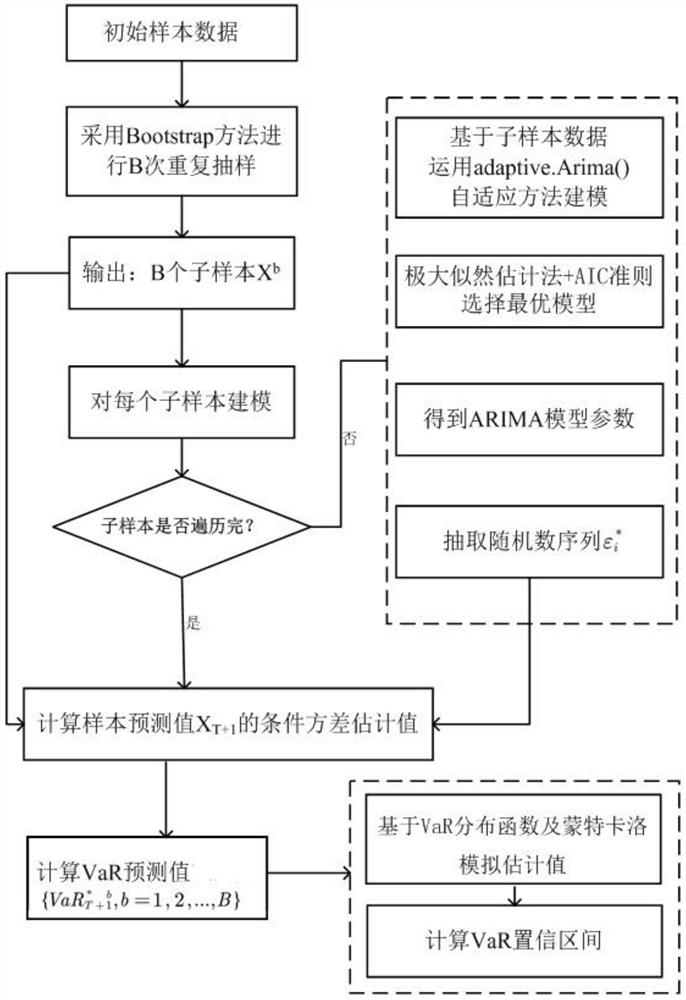

[0042] see figure 1 As shown, the VaR confidence interval prediction method combined with Bootstrap resampling and adaptive ARIMA model provided in this embodiment, the method is applied to the risk measurement of futures index in the financial market, including the following steps:

[0043] S1, use the Bootstrap method to repeatedly sample the initial sample data to generate Bootstrap sub-samples;

[0044] Using Bootstrap method to initial sample data {X t}Repeat sampling to generate sub-samples of Bootstrap b=1, 2,..., B, where the initial sample data {X t} with subsample The number of samples is the same, B is the number of samples, and n is the number of samples.

[0045] S2. The ARIMA model is gradually selected backwards, thereby calculating the ARIMA model parameters, and according to the obtained ARIMA model parameters, extracting a random number sequence subjec...

PUM

Login to View More

Login to View More Abstract

Description

Claims

Application Information

Login to View More

Login to View More