Loan program and process for transacting the same

a technology for transacting loans and short-term loans, applied in the field of short-term loan program and process, can solve the problems of not being able to meet such monthly obligations, people with little room, and not being able to adapt to emergencies, so as to achieve the effect of reducing the cost of transacting loans, reducing the cost of overall loans, and reducing the risks of loans

- Summary

- Abstract

- Description

- Claims

- Application Information

AI Technical Summary

Benefits of technology

Problems solved by technology

Method used

Image

Examples

Embodiment Construction

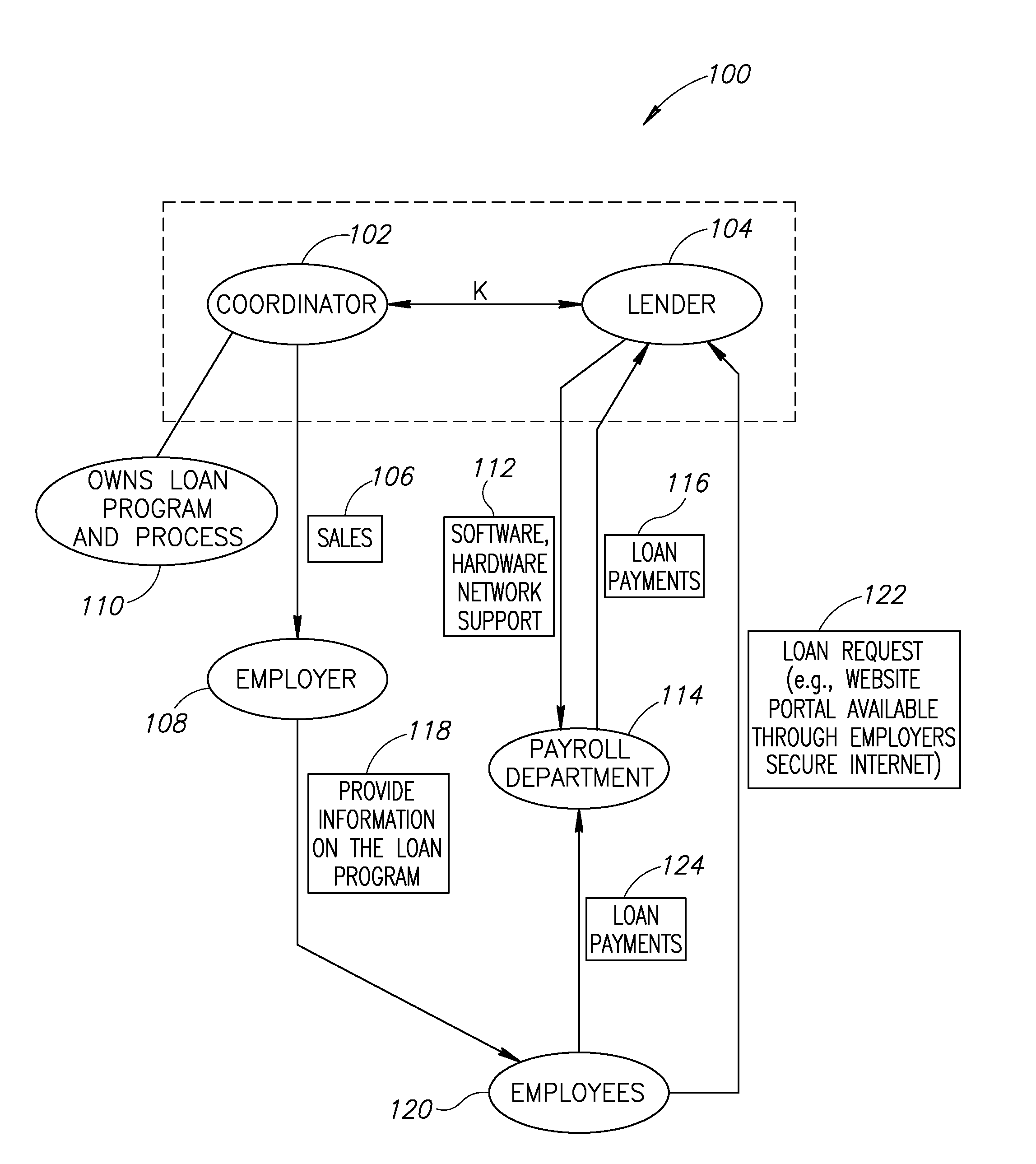

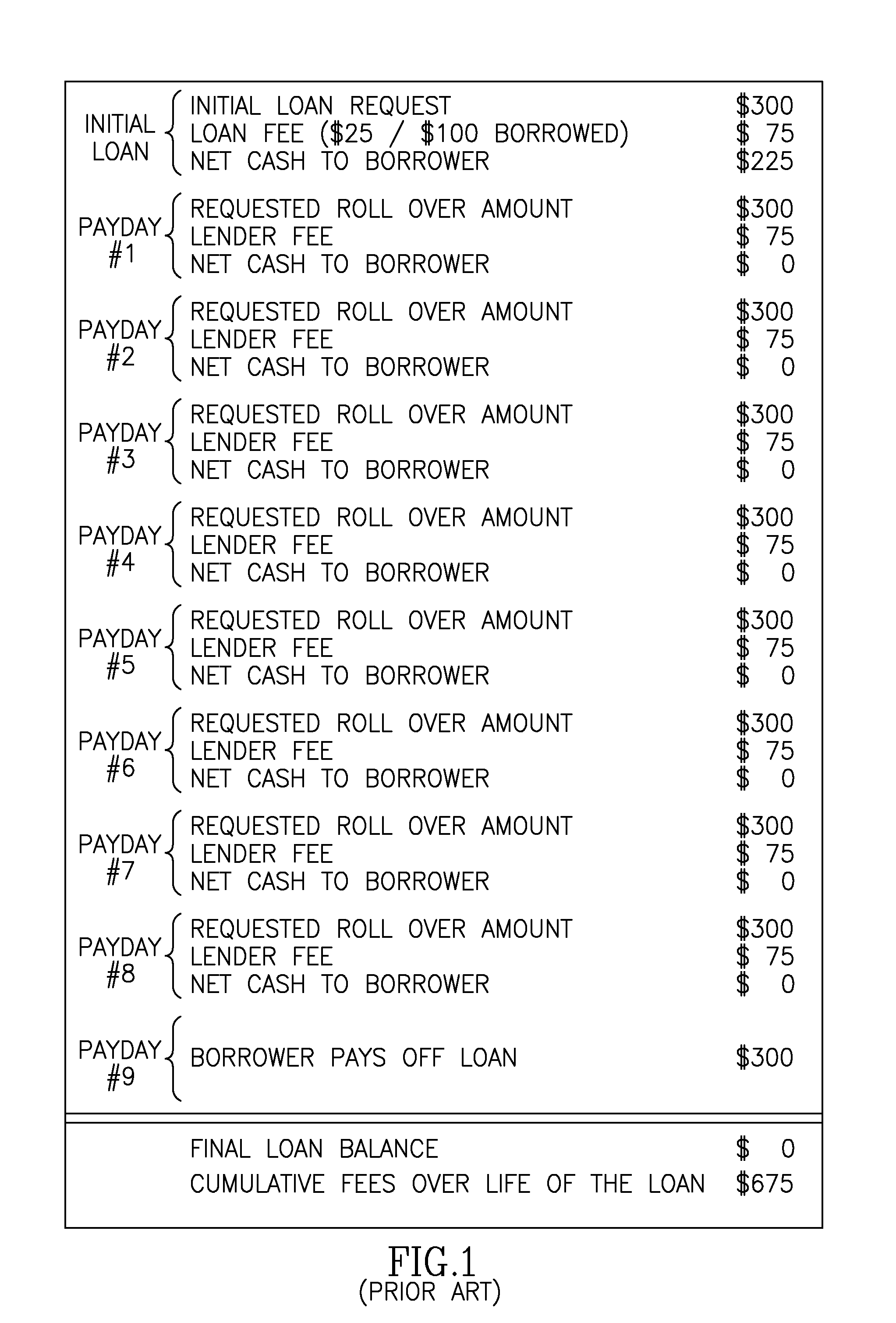

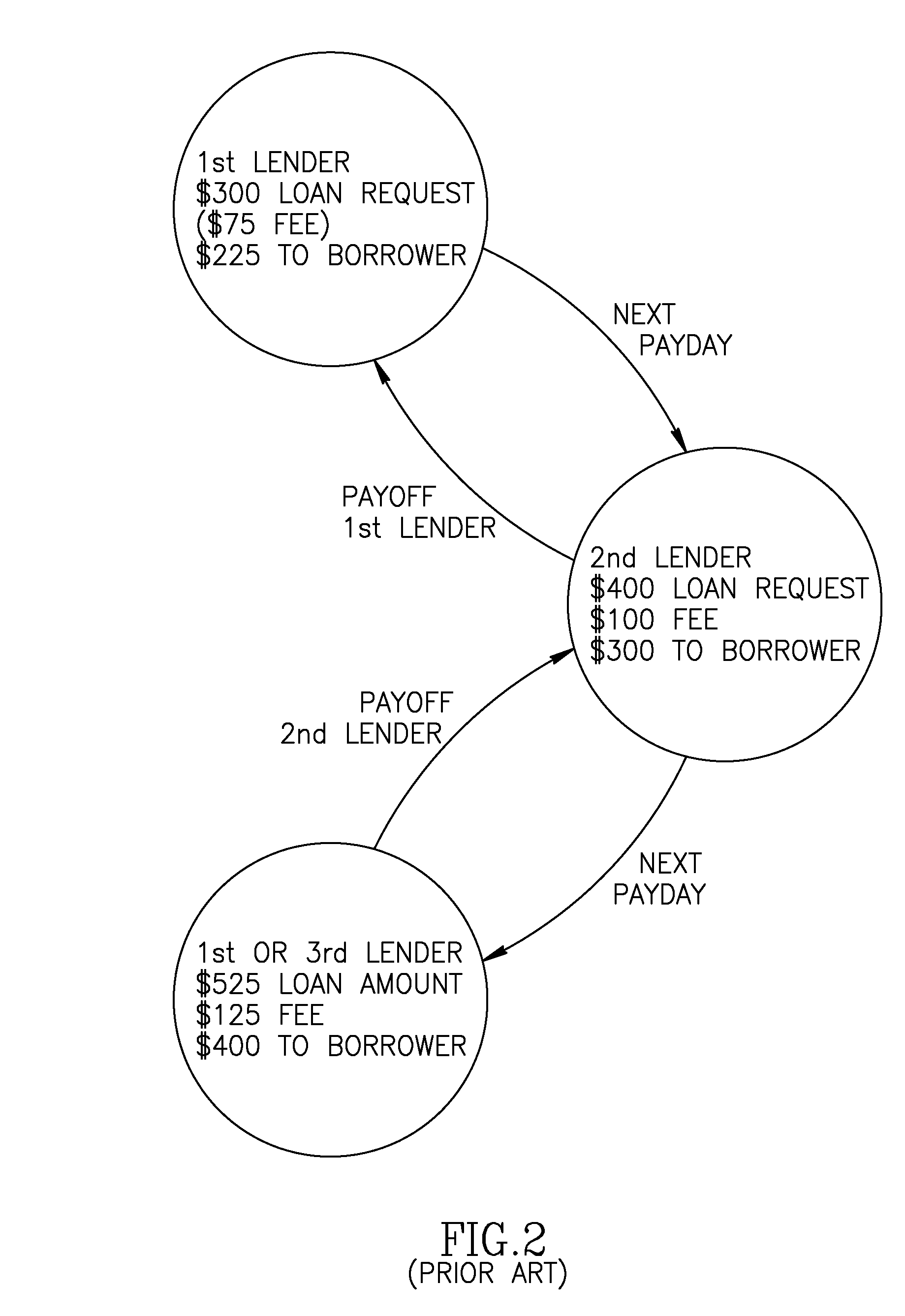

[0038]The present invention is generally directed to a loan program and process structured to provide significant end-to-end cost savings while overcoming many, if not all, of the drawbacks and regulatory obstacles present in the current payday loan industry and also overcoming many of the issues facing the conventional banking industry when attempting to process short term loans.

[0039]The complete process, from end-to-end, and the overall arrangement thereof, provides numerous advantages such as a lender's ability to offer short-term loans to employees through an employer controlled program where the employer specifies that the loans to the employees are to be provided at or below a fixed or agreed upon annual percentage rate (APR). In addition, the loan program and process is integrated with a payroll system of the employer to mitigate the risk of late or missed payments and ultimately mitigate the risk of loan defaults. As part of the integration of the loan program and process w...

PUM

Login to View More

Login to View More Abstract

Description

Claims

Application Information

Login to View More

Login to View More