An option pricing hardware accelerator

A technology of hardware accelerators and options, applied in instruments, computing with contact devices, computing with non-contact manufacturing equipment, etc., can solve problems such as difficult to guarantee computing performance.

- Summary

- Abstract

- Description

- Claims

- Application Information

AI Technical Summary

Problems solved by technology

Method used

Image

Examples

Embodiment Construction

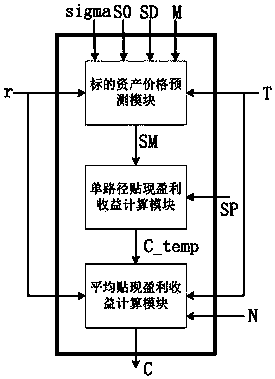

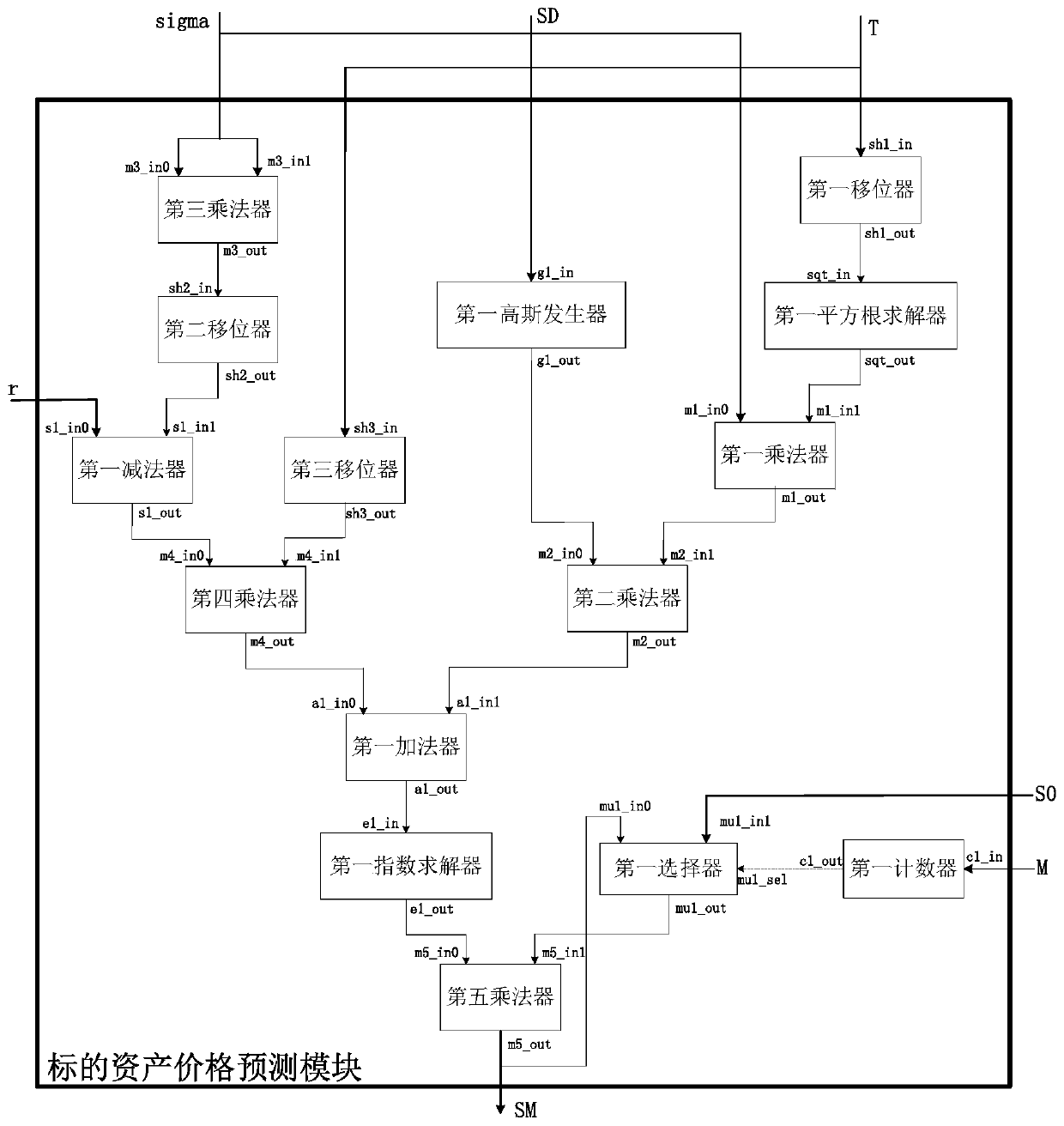

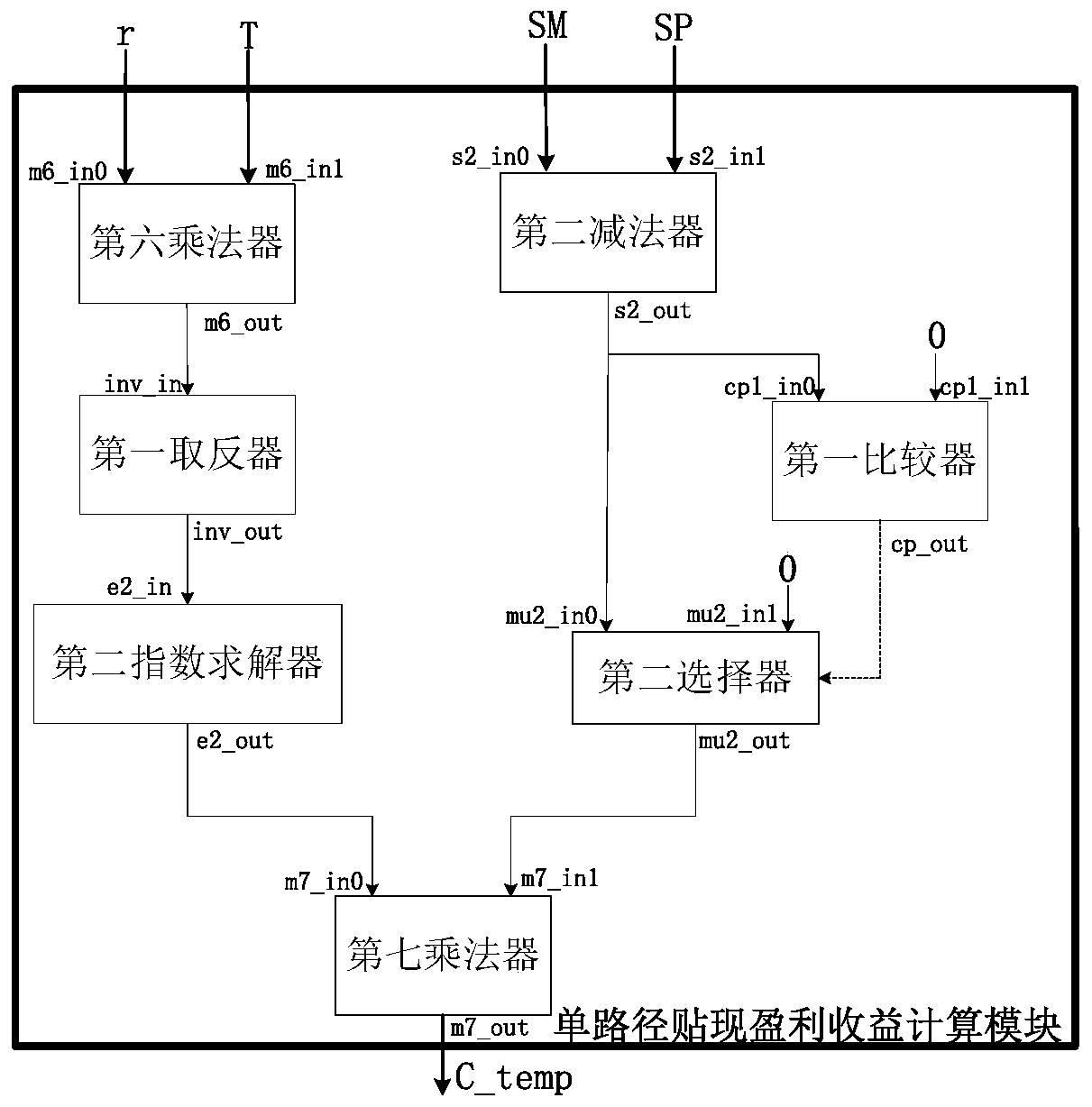

[0051] like figure 1 As shown, the option pricing hardware accelerator of the present invention is composed of a target asset price prediction module, a single-path discounted profit calculation module and an average discounted profit calculation module.

[0052] The option pricing hardware accelerator of the present invention has eight input ends and one output end; the eight input ends receive the configuration parameters of the option pricing hardware accelerator, which are: the input end of the risk-free interest rate parameter, the input end of the option validity period parameter, and the price volatility of the underlying asset. Parameter input terminal, the current market price parameter input terminal of the underlying asset, the exercise price parameter input terminal, the calculation iteration time point quantity parameter input terminal within the option validity period, the simulated sample path number parameter input terminal, and the seed input terminal of the Ga...

PUM

Login to View More

Login to View More Abstract

Description

Claims

Application Information

Login to View More

Login to View More